Time off for parental leave, necessity of paper ROEs, paying retirement allowances in instalments

Time off for parental leave

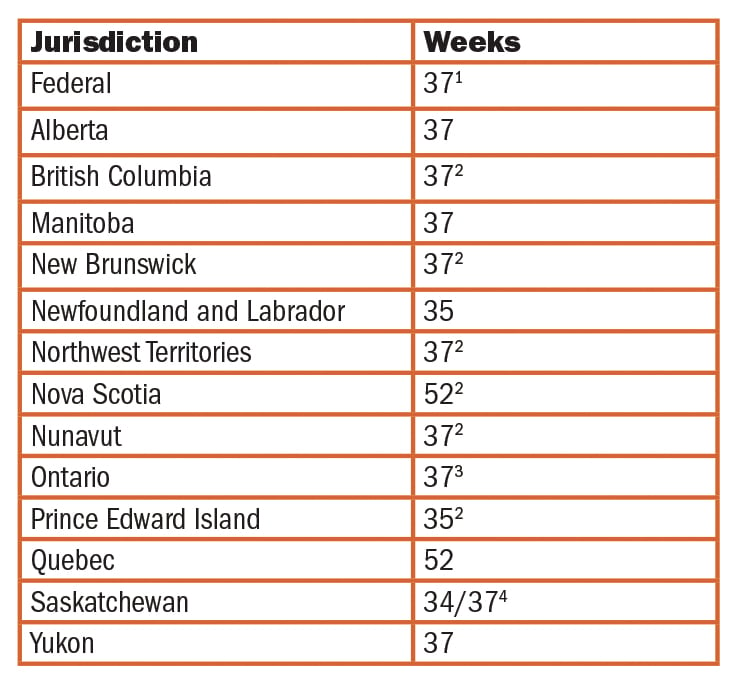

QUESTION: I understand that the federal government is changing the maximum period in which individuals may receive employment insurance (EI) parental benefits. Will this change affect unpaid parental leaves that employers must provide under labour standards law?

ANSWER: Recently passed federal legislation, which is not yet in force, will allow individuals claiming EI parental benefits to choose whether they want to receive the benefits for up to 35 weeks at a rate of 55 per cent of their average insurable weekly earnings or for a maximum of 61 weeks at a 33 per cent benefit rate.

The length of time individuals may receive EI parental benefits is not necessarily the same as the amount of unpaid time off that labour standards laws require employers to provide for a parental leave, although many jurisdictions do match their period of leave to the maximum length of EI parental benefits (and the benefits waiting period).

The federal government has also amended the Canada Labour Code to lengthen the maximum period of job-protected parental leave from 37 weeks to 63 weeks.

Once in effect, this amendment will apply to federally regulated workplaces.

It is expected that at least some provinces/territories will change their labour standards laws to increase the maximum number of weeks off that employees may take for a parental leave to match the federal changes.

In the meantime, employers must provide eligible employees with at least the time allotted in the table above.

Paper ROEs not necessary when filing electronically

QUESTION: A recently terminated employee is quite insistent that we have to provide him with a printed Record of Employment (ROE) even though we use an electronic ROE (ROE Web). Are we required to provide employees with a paper copy of the completed form?

ANSWER: No.

Employers who send ROEs electronically to Service Canada do not have to print a paper copy of the form for employees. The data on the form is transmitted to Service Canada’s database and it uses that information to administer employment insurance claims.

However, even though employers submitting electronic ROEs are not required to provide a printed copy of the form to employees, Service Canada recommends that employers do so as a courtesy.

It adds that employers should inform the individuals that they have submitted the form electronically and, therefore, the employees should not provide Service Canada with a printed copy of it.

Service Canada also advises that individuals registered with the government’s online service called My Service Canada Account may view and print copies of their electronic ROEs.

It may be helpful to let employees know this and suggest they sign up for the service at Service Canada’s website at www.canada.ca/en/employment-social-development/services/my-account.html.

Paying retiring allowances in instalments

QUESTION: We are paying severance pay to a long-service employee whose position has been eliminated. We are paying it in two instalments. Does the payment still qualify as a retiring allowance even though we are not paying it in a single payment?

ANSWER: Yes, severance pay can be paid in instalments and still qualify as a retiring allowance. To ensure that the payment is a retiring allowance, make sure that the employee is not allowed to continue to accrue pension credits (if applicable) after the termination. That would disqualify the severance pay as a retiring allowance.

It is also important to check the employer’s benefit plan to see if continued participation is limited to employees only. If so, the company would need to have or establish a plan specifically for non-employees such as retirees or terminated employees. Otherwise, if benefit coverage is continued after termination, the severance payment would be disqualified as a retiring allowance.

Retiring allowances are not subject to Canada/Quebec Pension Plan contributions, employment insurance premiums or Quebec Parental Insurance Plan premiums, with the exception of legislated wages in lieu of notice payments. Retiring allowances are taxable with income tax deductions calculated using the lump-sum tax rates.

Those with years of service before 1996 may transfer part or all to a registered pension fund or registered retirement savings plan in which they are the annuitant to avoid income tax deductions.