‘The financial impacts last well beyond the period of care provision’

HR professionals who overlook the cost of unpaid caregiving risk locking female employees into retirement poverty, a new World Economic Forum (WEF) report warns.

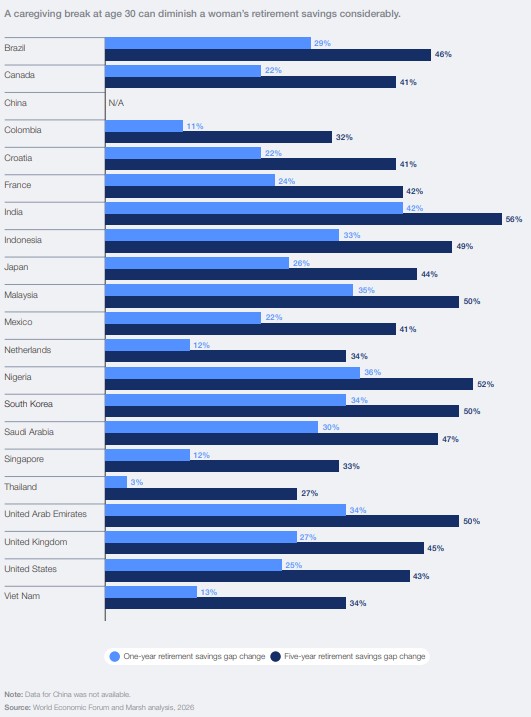

The report notes that a five-year caregiving break combined with Canada's gender wage gap can erase 41 per cent of a woman's retirement savings.

The Longevity Dividend: The Business Case for Linking Health and Wealth, published in June 2026 with Marsh, draws on analysis across 21 countries to argue physical and financial health are inseparable and that employers leave trillions in savings unaddressed.

Caregiving penalty in Canada

In Canada, a single year of caregiving leaves a 22 per cent retirement savings gap between women and men — rising to 41 per cent after five years.

“Caregiving can occur at any stage of life, from parents who care for infants to adults who help ageing or sick loved ones,” reads part of the report. “Regardless of when it happens, the financial impacts last well beyond the period of care provision, and as populations live longer, those impacts compound.”

The gap locks in around age 30 — the average first-birth age in OECD countries — before women reach their peak earning decade. Globally, more than 700 million women are prevented from entering labour markets due to care duties, against 40 million men.

Overall, 47 per cent of Canadians identify as caregivers—whether parenting young children, caring for elderly relatives, or supporting individuals with special needs—according to a previous Mental Health Research Canada (MHRC) study. These individuals experience significantly higher rates of burnout (31 per cent versus 23 per cent among non-caregivers), financial stress (40 per cent versus 34 per cent), and increased demand for mental health support compared with their non-caregiving counterparts.

“Caregiver-employees report increased burnout and are almost twice as likely to have mental-health-related absences, underscoring the need for employer support,” according to one expert.

Ageism and productivity losses

Also, Canada stands to lose $7.53 billion (USD) in cumulative productivity between 2025 and 2040 from the under- and unemployment of workers aged 55 and over, against $113.51 billion (USD) for the United States and nearly $500 billion across OECD countries, according to the WEF.

Workers aged 55 and over spend an average of seven additional weeks unemployed compared with younger counterparts, and many leave the labour force without appearing in unemployment data. The report recommends employers counter ageism through multigenerational hiring and retention practices.The WEF models three preventative health interventions — home fall-proofing, increased physical activity and expanded hearing aid access — projecting more than $5.8 trillion in healthcare savings globally by 2040.

Fall-proofing Canadian homes is projected to deliver $73 billion (USD) in benefits, against $409 billion for the United States, on a $393 billion global outlay.

On hearing aids, Canada is projected to recover 162 per cent of its initial cost through dementia-related savings — against 106 per cent for the United States. Canadian healthcare savings reach nearly $6 billion (USD), against $66.78 billion for the United States and $327.42 billion globally.

"Governments that fund preventative health programs from one ministry and plan overall country finances from another will face structural barriers to tackling the larger, interrelated challenges associated with longevity," the report states, calling on HR, finance and occupational health to operate from a shared longevity framework.

Recently, the Ontario Superior Court dealt with a case involving age discrimination when an Ontario manufacturer decided to close one plant and move operations just over 100 kilometres away.

Reversing the penalty

The WEF describes the caregiving penalty as the product of structural policy choices. France and Germany are cited as models with caregiver credits that let caregivers keep accumulating pension benefits — an approach the report urges Canadian employers to adapt.

The table below compares the three countries across the key design features of their caregiver pension credit systems.

|

Feature |

Canada (CPP) |

France |

Germany |

|

Program name |

Child-Rearing Provision (CRDO) / CPP Enhancement Drop-in |

Assurance vieillesse des parents au foyer (AVPF) + supplementary Agirc-Arrco top-ups |

Kindererziehungszeiten (KiZ) — child-rearing pension credits |

|

Year introduced |

Child-rearing provision: 1977; CPP Enhancement drop-in: 2019 |

1945 (child pension bonus); expanded 1972 and subsequently |

1986; expanded 2001 and 2025 |

|

Covers child caregiving |

Yes — primary caregiver of child under age 7 |

Yes — parent caring for child under age 3 (AVPF) and broader credits for children up to age 16 |

Yes — up to 3 pension points (one per year) for children born after 1992; 2.5 points for children born before 1992, equalised to 3 points under 2025 reform |

|

Covers eldercare / adult caregiving |

No CPP pension credit for eldercare. Canada Caregiver Credit (CCC) is a non-refundable income tax credit only (up to $8,601 for 2025), not a pension accrual benefit |

Yes — caregivers providing substantial care to a disabled, sick or elderly person at home can access pension contributions under certain conditions |

Yes — family caregivers providing at least 10 hours of care per week receive pension contributions paid by the statutory long-term care insurance fund (Pflegeversicherung) |

|

How the credit works |

Low or no earnings during eligible period are "dropped out" of the CPP benefit calculation, or "dropped in" with credits based on the caregiver's average earnings in the 5 years prior to the caregiving period (CPP Enhancement, post-2019) |

State pays social insurance contributions to the CNAV (national pension fund) on behalf of eligible caregivers, crediting them as if they were employed |

Caregiving periods are counted as insured employment periods; pension points are credited directly to the caregiver's statutory pension account |

|

Pension credit value |

Drop-in credits based on pre-caregiving average earnings (CPP Enhancement component only; base CPP uses dropout, not drop-in) |

Contributions based on a reference wage — historically 169 times the hourly minimum wage per month, updated annually |

1 pension point per year per child (post-1992 births); equivalent to the pension entitlement of a person earning exactly the average national wage for one year |

|

Maximum duration |

From the month after the child's birth until the child turns 7; if multiple children, the period runs continuously until the youngest turns 7 |

Up to 3 years per child under the AVPF child component; eldercare credits apply for the duration of qualifying care |

3 years per child (post-1992); caregiving for sick/elderly adults covered for as long as the qualifying care relationship continues |

|

Application required |

Yes — must be applied for; not automatic. Applied for at the time of CPP benefit claim or via a separate form |

Largely automatic for parents receiving family allowances; caregivers of adults must register separately |

Largely automatic through the long-term care insurance system for eldercare; child credits applied through the pension insurance system |

|

Both parents eligible |

One parent at a time; the parent who received the Canada Child Benefit is the default; can be waived to the other parent |

Credits can be split between parents in some circumstances |

Both parents may receive credits simultaneously under certain conditions; primary caregiver receives the full credit |

|

Gap: eldercare pension accrual |

Significant gap. No CPP pension accrual mechanism exists for workers who reduce hours or leave the workforce to care for an ill or elderly adult. EI caregiving benefits provide short-term income replacement only (up to 35 weeks for family caregiver benefit) |

Partial coverage — conditions and duration of eldercare pension credits are more limited than child-rearing credits |

Strongest coverage. Germany's long-term care insurance system funds pension contributions for family caregivers of adults, providing ongoing pension accrual for the duration of qualifying care |

"When care counts, employers come to see caregiving breaks as retention opportunities rather than accommodation," the report states, calling on employers to create return-to-work pathways and design benefits that explicitly offset lost retirement contributions.

Women tend to live longer, earn less and carry greater caregiving loads than men — a gap the WEF says raises older-age poverty risk and flows back to employers as reduced workforce participation.