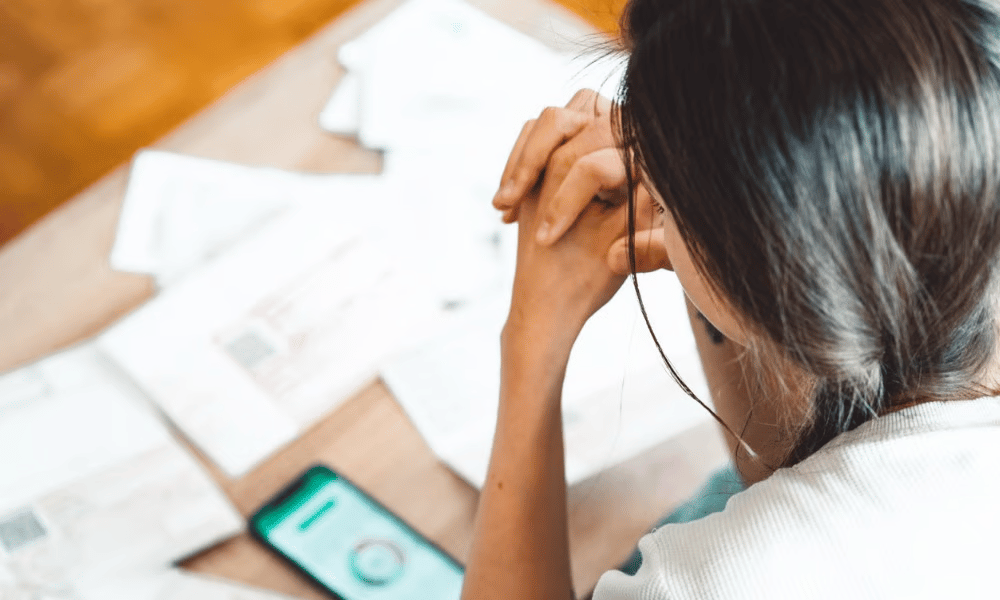

‘Many Canadians are... entering each pay period with much of that paycheque already committed before it arrives’

Many Canadians are dealing with significant financial stress, according to a recent report.

Three in five (61%) say at least half of their income is already committed to bills, debt payments, and regular expenses before their paycheque arrives, reports insolvency firm MNP.

A third (32%) say most of their paycheque is spoken for in advance, and one in six (16%) say all of it is committed or that expenses exceed upcoming income.

“Many Canadians are not just living paycheque to paycheque, they are entering each pay period with much of that paycheque already committed before it arrives,” says Grant Bazian, president of MNP.

“The difference is that the next paycheque is not a reset point. It is already assigned to bills, debt payments, and regular expenses. That may help people stay current in the short term, but it can also create a rolling shortfall, where each paycheque is used to catch up from the last one. This leaves households more vulnerable when costs rise, income changes, or debt payments become harder to manage.”

A majority of workers are distracted by financial problems while at work, according to a previous report. Also, about 7.3 million adult Canadians are doing gig work, with many citing the need to do so to meet rising costs.

Index rises modestly but vulnerability persists

The MNP Consumer Debt Index - measures Canadians’ attitudes toward their consumer debt and gauges their ability to pay their bills and endure unexpected expenses, among others - climbed to 91 points, up four from last quarter, MNP said.

Three in 10 Canadians (30%, unchanged) expect their debt situation to improve within a year; two in five (40%, up three points) expect improvement within five years.

Nearly half of Canadians (46%) report being $200 or less from insolvency monthly, up three points. Almost three in 10 (28%) do not earn enough to cover bills and debt.

Households cutting back on family, social spending

Still, more than one in three Canadians (35%) are cutting back on family and personal enrichment expenses, including personal care and children's activities, MNP said.

More than half (57%) are cutting back travel and experiences, and 56% are cutting dining and socialization, including 48% on restaurants or takeout. Nearly a quarter (23%) are cancelling plans entirely.

"Many are shrinking parts of their lifestyle to keep up with the cost of essentials," Bazian said. "It can weigh on overall quality of life and emotional well-being."

The Bank of Canada has held its key rate steady this year, but MNP data suggests limited room to absorb increases.

Framed as an additional $130 in monthly interest, only one in five Canadians (21%) say they could manage the cost, while more than a third (35%) could not absorb it.

Three in five (62%, up one point) say they need rates lowered, and more than half (53%) fear financial trouble if rates rise.

Warning signs of financial stress

Bazian said warning signs of financial distress may not always resemble a missed payment or collection call. A household may appear to be managing by cutting back or relying on credit while still moving deeper into a rolling shortfall, MNP said.

“Financial stress no longer stays on a spreadsheet. It moves into sleep, focus, mood and resilience, and eventually into absenteeism, disability claims and turnover,” according to Beneva.

“In a Canadian context shaped by persistent inflation, housing pressure, economic uncertainty and an aging workforce, financial strain has become one of the most influential health determinants in the workplace.”