Probationary employees, source deduction remittance schedules

Keeping records for probationary employees

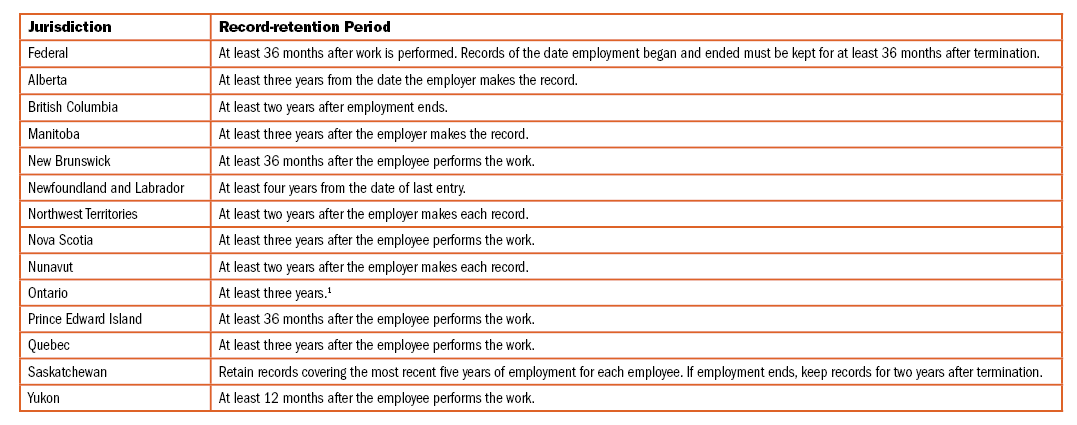

QUESTION: For how long are employers required to keep records on employees who quit or whose employment is terminated while they are on probation?

ANSWER: The period for which employers have to keep employment records is the same regardless of whether an employee is on probation.

For labour standards purposes, the minimum period for keeping records depends of the jurisdiction in which the employee is employed. For detailed analysis, please refer to the chart above:

NOTE

1 The timing of the three-year period varies, depending on the type of record:

• Employee’s name, address and, starting date of employment: three years after termination.

• Employee’s date of birth if the employee is a student under 18 years of age: earlier of three years after the employee turns 18 or termination of employment.

• Work hours: three years after the day or week of work.

• Agreements to work excess hours or average overtime pay: three years after the last day on which the employee worked under the agreement.

• Vacation time and pay: three years after the employer makes the record.

• Unpaid leaves of absence allowed under the Employment Standards Act, 2000: three years after the day the leave ended.

The Canada Revenue Agency and Revenu Quebec require employers to keep payroll records of earnings subject to source deductions and employer contributions for a minimum of six years after the tax year to which they apply.

Employers must keep payroll records related to a Record of Employment (ROE) for six years after the year to which it covers. Employers using print ROEs must keep part 3 of the form for six years after the year to which the information on the ROE relates. Employers using electronic ROEs, such as ROE Web, do not have to store paper copies of forms they have issued. For the Quebec Parental Insurance Plan, employers must retain the form Relevé de renseignements sur l’emploi—Régime québécois d’assurance parentale for six years after the year to which it covers.

Determining source deduction remittance schedules

QUESTION: We are switching from a monthly payroll to a bi-weekly one. Will this affect our schedule for sending source deduction remittances to the Canada Revenue Agency (CRA)?

ANSWER: No, an employer’s CRA remittance schedule is not related to the type of pay period it uses. To determine an employer’s source deduction remittance schedule (with the exception of quarterly remitting), the CRA looks at the employer’s average monthly withholding amount (AMWA) from two calendar years ago (for instance, 2017 remittances are based on the employer’s average monthly remittance in 2015). The average is obtained by dividing the total amount of CPP, EI and income tax the employer had to remit by the number of months (to a maximum of 12) for which it had to remit.

To be eligible for quarterly remitting, the CRA requires employers to have an AMWA of under $3,000 in the first or second preceding calendar year, as well as a perfect record for sending in remittances (including GST/HST remittances) and T4 and GST/HST returns in the last 12 months.

The CRA will notify employers who qualify for quarterly remiting.

The CRA allows new small employers to send in their remittances quarterly if their monthly withholding amount is less than $1,000 and they have a perfect compliance record with the CRA over the previous 12 months. These employers do not have to first obtain the CRA’s permission to remit quarterly. The agency says they can send in remittances on a quarterly basis unless it notifies them otherwise.