Understanding maternity leave benefits, taxable benefits from supplier discounts, subsidized cafeterias

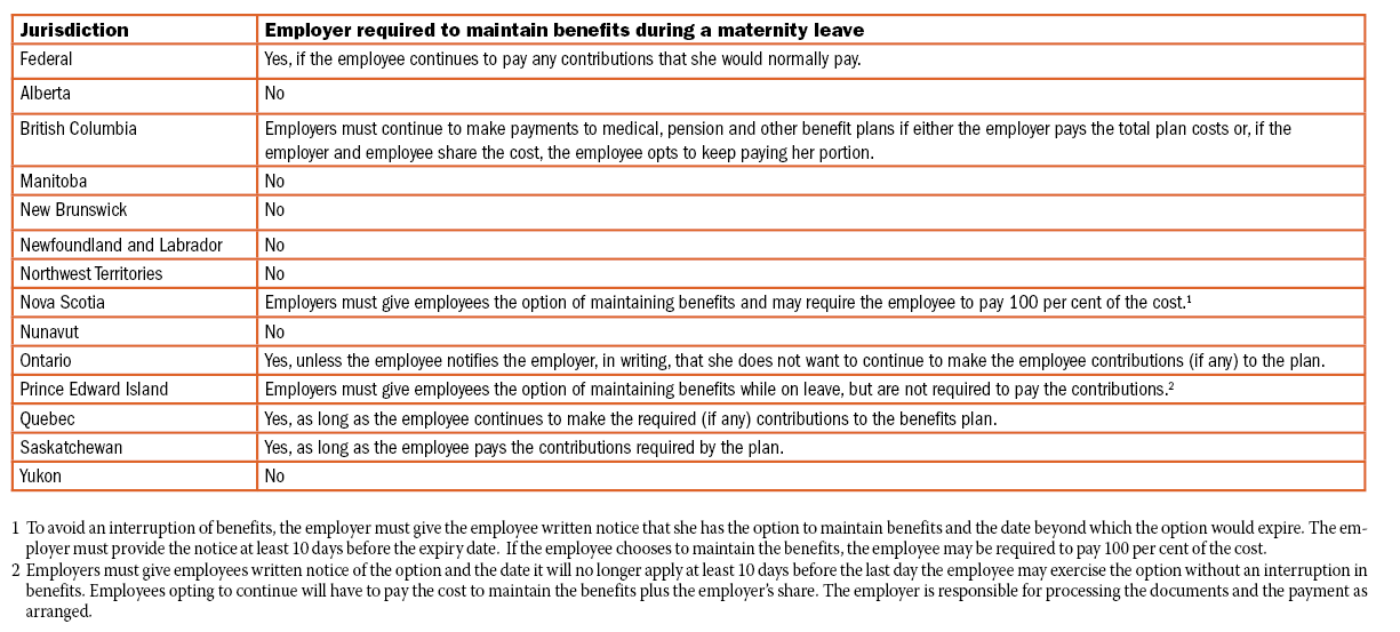

Maintaining benefits during a maternity leave

QUESTION: Are employers required to continue benefits coverage (such as dental or prescription drugs) for employees who are on an unpaid maternity leave?

ANSWER: The answer depends on the jurisdiction in which the employees work, since maternity leave requirements are governed by provincial/territorial labour standards and the Canada Labour Code for federally regulated workplaces. Refer to the table above:

Taxable benefits from supplier discounts

QUESTION: One of our suppliers has offered to provide a discount to any of our employees who purchase items from them as a way to say thank you for the amount of business we give them. They sell laptops and related supplies. Are there any taxable benefit issues that could arise from this or do the taxable benefit rules not apply since it is the supplier offering the discount and not the employer?

ANSWER: Even though the supplier is not the employer, a discount that it offers to an employer’s staff will result in a taxable benefit to the employees if the supplier does not also offer the discount to the public at large or to specific public groups.

The Canada Revenue Agency (CRA) says that the basis for this comes from s.6(1)(a) of the federal Income Tax Act, which states that an individual’s employment income generally includes the value of benefits “of any kind whatever received or enjoyed by the taxpayer in the year in respect of, in the course of, or by virtue of an office or employment.”

In Income Tax Folio S2-F3-C2, Benefits and Allowances Received from Employment, the CRA explains that it interprets the phrase “in respect of employment” broadly, meaning that an employer may have to include benefits in an employee’s income even if the employer was not the one who provided them.

If a taxable benefit arises from a third-party discount, the value of the benefit would be the fair market value of the item(s) that the employee bought from the supplier (including the GST/HST/QST, as applicable), less the amount the employee paid.

If the supplier also provides the discount to the general public or to specific public groups, the CRA states that the discount would then not be a taxable benefit for the employees.

Should employer-subsidized cafés be a taxable benefit?

QUESTION: We recently opened a cafeteria for employees at our office. Both employees and visitors are welcome to use it. The food served is not free, although we do subsidize it to encourage employees to use it. Is this a taxable benefit?

ANSWER: The CRA advises that meals provided to employees in employer cafeterias are not taxable benefits if the amount that the employees pay for the food is reasonable. When considering if the amount paid is reasonable, the CRA says it takes into account how much it costs to buy the food, prepare it and serve it.

If the amount the cafeteria charges is unreasonably low, a taxable benefit will arise.

The value of the benefit will be the cost of the meals (including the GST/HST/QST) less any amount that the employee paid for them. If taxable, besides income tax deductions, the benefit must be included when calculating Canada/Quebec Pension Plan contributions. Do not include the taxable benefit when calculating Employment Insurance or Quebec Parental Insurance Plan premiums since the meal would be a non-cash benefit.

At year end, include the value of the taxable benefit in box 14 on the employee’s T4, as well as in the “Other information” area, using code 40. For Quebec employees, also report the taxable benefit in boxes A and V on an RL-1.