'Lower income households are more likely to benefit from declining interest rates, as they tend to be more indebted relative to higher income households'

The income gap between Canada’s wealthiest and poorest households reached a record high in the first quarter of 2025, reports Statistics Canada (StatCan).

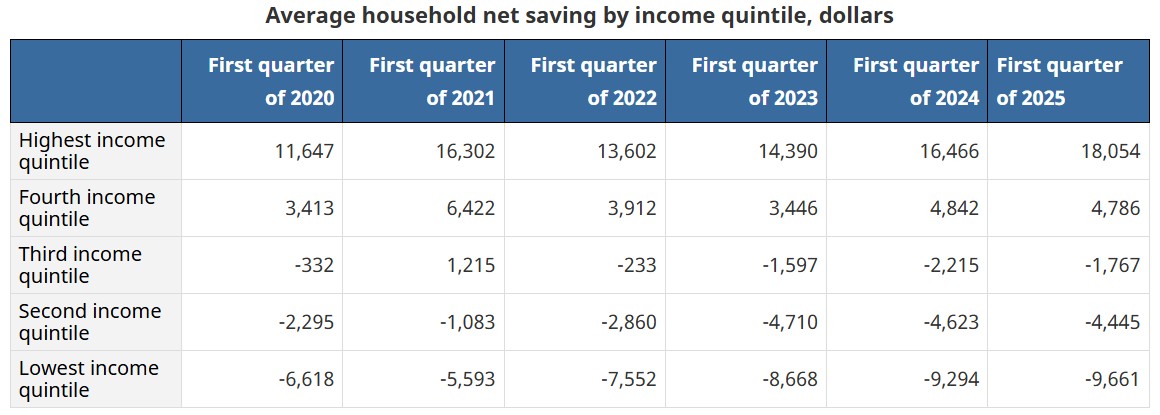

The difference in disposable income share between the top 40 per cent and bottom 40 per cent of Canadian households hit 49 percentage points, the widest gap since tracking began.

The figure has jumped from 43.8 points in early 2021, with the gap expanding each year since the COVID-19 pandemic.

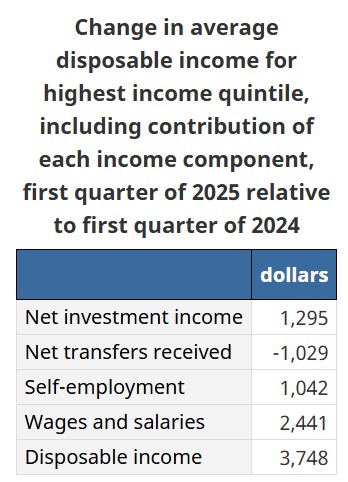

The Q1 2025 data resulted from top earners benefiting from investment gains, while the lowest-income households saw their wages decline.

Households' ability to maintain their economic well-being varies with macroeconomic conditions, StatCan notes. In contrast with prevailing high interest rates in 2023, the Bank of Canada reduced its policy rate from 5.0 per cent in April 2024 to 2.75 per cent in March 2025 in response to easing inflationary pressures.

Along with declining interest rates, household interest payments decreased for the first time since 2022, falling by 4.8 per cent in the first quarter of 2025 relative to the first quarter of 2024, notes StatCan.

“While declining interest rates can lead to easing borrowing costs for households, they can also lead to lower yields on interest-bearing investments, such as savings and deposit accounts,” it says. “Lower income households are more likely to benefit from declining interest rates, as they tend to be more indebted relative to higher income households. However, they also tend to have less diversified investment portfolios that focus on interest-bearing instruments rather than other forms of investments, such as equities.”

Several provinces and territories have already increased their base pay rates earlier this year, and more will follow suit come October.

Job loss among lower income households

Lower income households also tend to be more susceptible to job loss during economic downturns, according to the StatCan report.

Citing data from the Labour Force Survey, StatCan notes that the employment rate—the proportion of the population aged 15 years and older who are employed—has been on a declining trend since early 2023.

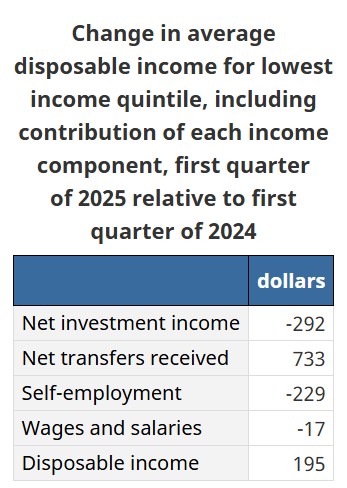

“The lowest income households (bottom 20 per cent of the income distribution) had the weakest growth in disposable income in the first quarter of 2025 relative to one year earlier (+3.2 per cent). This is because they were the only group that had declining average wages (-$17; -0.7 per cent), due mainly to reduced hours of work. Labour market conditions were notably weak for people working in mining and manufacturing.

“The lowest income households also had the largest reduction in net investment income, as a decline in investment earnings (-$399; -35.3 per cent) more than offset lower interest payments (-$107; -7.1 per cent).”

Meanwhile, households in the middle 60 per cent of the income distribution increased their income at a below-average pace in the first quarter of 2025 relative to one year earlier (+4.9 per cent compared with +6.0 per cent for all households).

How to improve workers’ financial wellbeing

Financial support is one of the hottest employee benefits in Canada right now, according to a previous report.

“Financial wellness has moved from a buzzword to a business imperative,” says Eric Paley, leader of Nixon Peabody’s employee benefits team.

“With economic uncertainty, rising inflation, and growing employee stress, employers are rethinking how they support their workforce beyond traditional retirement plans. Financial wellness programs are emerging as a key strategy to improve employee engagement, reduce turnover, and enhance overall benefit value.”

To maximize the value of financial wellness programs, he notes that employers should:

- Engage vendors with a fiduciary mindset, even if the program is not subject to ERISA.

- Offer opt-in participation, rather than mandatory enrolment, to respect employee autonomy.

- Communicate clearly about the program’s purpose, scope, and limitations.

- Track utilisation and outcomes to assess ROI and make data-driven improvements.