Want to help your employees claim tax credits on eligible medical expenses? Read this guide for HR best practices and CRA-compliant reimbursement policies

Air conditioner. Gluten-free food products. Moving expenses. Renovation costs. Whirlpool bath treatments.

Not many people know that these could count as eligible medical expenses and qualify for tax credits. Experts say that this might be among the most underused tax benefits among Canadians. Could your employees be missing out on potential tax savings?

In this article, we’ll give an overview of the medical items that your employees can claim tax credits on. We’ll share some best practices on how HR teams can educate the workforce about these benefits, and how that could benefit the organization.

What medical expenses are tax deductible in Canada?

Medical expenses aren’t tax deductible per se; in Canada, eligible medical expenses qualify for a medical expense tax credit (METC). The METC is a non-refundable tax credit that reduces the amount of taxes owed.

The Canada Revenue Agency (CRA) website lists over 100 health and medical items that qualify for these tax credits. Here’s a quick look at some of these approved medical expenses:

1. Attendant care and care in a facility

Eligible medical expenses

-

Attendant care services: Salaries and wages paid for services in facilities like private homes, retirement homes, group homes, and nursing homes

-

Full-time care: Entire costs for full-time care in nursing homes, including accommodation, meals, nursing care, administration, maintenance, and social activities

Conditions

There are exclusions and detailed guidelines for this expense. Employees can visit the CRA website for guidance or chat with a live agent by logging into My Account.

2. Care, treatment, and training

Eligible medical expenses

-

Care and treatment for certain transplants, treatments, surgery or procedures

-

Costs for therapy sessions, including speech, occupational, and physiotherapy, when prescribed by a medical practitioner

-

Training to learn how to care for a relative who is mentally or physically impaired

Conditions

-

Training costs should be reasonable and paid to someone who isn’t a spouse or common-law partner

-

A prescription or certification is required for certain therapies and treatments

3. Construction and renovation

Eligible medical expenses

-

Home modifications: Expenses in renovating a home to accommodate a person with a disability. Some examples: installing ramps, widening doorways, or modifying bathrooms

-

Purchase of a furnace: Cost of an electric or sealed combustion furnace if this is required due to an occupant’s chronic respiratory illness or immune disorder

Conditions

-

Modifications must be needed to allow the individual to gain access to or be mobile within the dwelling

-

A medical practitioner's certification may be required

Employees seeking to claim tax credits on these expenses should keep all receipts and related documents.

Renovation expenses should be reasonable. These should not be expected to raise the property value of the home.

4. Devices, equipment, and supplies

Eligible medical expenses

-

Purchases of medical devices, equipment, and supplies prescribed by a medical practitioner, such as wheelchairs, hearing aids, artificial limbs, and oxygen equipment

-

For kidney machines, cost of purchase, repairs, and maintenance also qualify

Conditions

-

Most items on the list require a prescription or certification

5. Gluten-free food products

Eligible medical expenses

-

The price difference between gluten-free food products and similar food items with gluten

Conditions

-

A medical practitioner must certify in writing that the individual has celiac disease and requires a gluten-free diet

-

Claims should be supported by receipts and a summary of the cost difference compared to non-gluten-free products

6. Prescribed drugs, medications, and other substances

Eligible medical expenses

-

Medication and devices bought under health Canada’s Access Program

-

Costs for prescription medications and drugs prescribed by a medical practitioner and recorded by a pharmacist

-

Medical cannabis purchased according to regulations

Conditions

-

Over-the-counter medications, even if prescribed, are not eligible

7. Service animals

Eligible medical expenses

-

Costs for buying and taking care of service animals trained to assist people with disabilities

-

Expenses for the animal's care, including food, veterinary care, and training

Conditions

-

The animal must be specially trained to help with the person’s impairment

-

A medical practitioner's certification may be required

8. Services and fees

Eligible medical expenses

-

Payments to medical practitioners, including doctors, dentists, and nurses, for medical services

-

Fees for laboratory tests, diagnostic procedures, and ambulance services

-

Medical services at a licensed hospital outside Canada is also allowed

Conditions

-

Services must be provided by authorized medical practitioners

9. Travel expenses

Eligible medical expenses

-

Travel costs for medical services not available within 40 kilometres of the individual’s home

-

If the distance is over 80 kilometres, additional expenses such as accommodation, meals, and parking may be claimed

Conditions

-

Similar medical services are not available near the individual’s home

-

It is reasonable for the individual to travel for the medical service

-

The most direct route and lowest available fares are to be used

-

If the individual cannot travel alone, a companion’s travel expenses can be claimed if there’s a medical certification

Detailed guidelines and conditions for all expenses are on the CRA website.

Is it worth claiming medical expenses on taxes in Canada?

It’s worth the effort if your employees spend a lot on health and medical needs for themselves and their families.

Canada Revenue Agency sets a medical expense threshold. For 2024, it is:

- three percent of net income or

- $2,759, whichever is lesser

If an employee’s expenses fall below this threshold, the effort to claim the tax credit may not be worthwhile.

Here’s the good news: there are more items on the CRA’s list of eligible medical expenses than most people realize. Also, claims can be made on a spouse’s return if their income is lower, which can increase the benefits.

HR teams can play a key role in raising awareness of this tax credit. This can help employees make the most of what is available to them.

How to claim medical expenses

Once your employees know which medical expenses are eligible, they’ll need help understanding how to claim them correctly. Here's how you can guide them through the process.

Be clear on what medical expenses benefits you offer

If your organization offers a private health services plan (PHSA) or a health spending account (HSA), make your employees aware of these benefits. (According to a 2023 survey, an HSA is one of the top benefits that employees look for.)

You’ll want to specify if the employer sponsors the PHSA or HSA in full, or if the employee pays partial premiums.

Employees’ medical claims under PHSA or HSA are valid if they are part of CRA’s list of qualifying health-related expenses. Because employees get reimbursed under the PHSA or HSA, they should not include these medical expenses in their tax returns.

Share instructions for claiming tax credits

If your employee pays eligible medical expenses out of pocket, they can include these on their tax form.

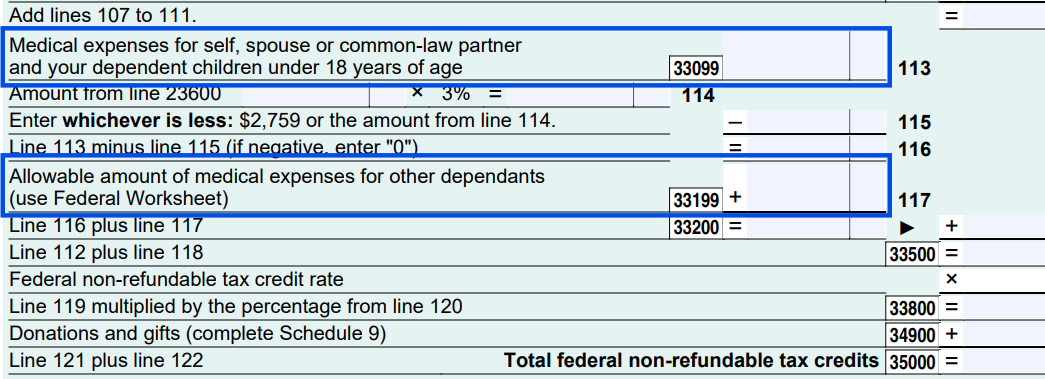

They’ll need to look out for lines 33099 and 33199 under Step 5 of their income tax and benefits return:

Line 33099 is used to claim total qualifying medical expenses paid by:

- the employee

- their spouse or common law partner

- their children under 18 years old

Line 33199 is used for allowable medical expenses of other dependants, such as:

- employee and their spouse’s/common-law partner’s children over 18 years old

- grandchildren

- parents

- siblings

- aunts/uncles

- nephews/nieces

Your employees will need to deduct the medical expense threshold set by CRA from these figures.

Refer your employees to CRA’s page on how to claim medical costs for tax credits.

Prepare documentation to help employees claim tax credits

Having the right paperwork at the start of the tax season goes a long way in helping your employees. Get these documents ready for them:

T4 slip

Code 85 on the T4 slip records health plan premiums paid by the employee. While optional, including Code 85 can be a big help to your employees. It can prevent the CRA from getting in touch with your employees for additional documentation.

There’s no need to use Code 85 if the employer pays the premiums in full.

Year-end benefit summary

This is a record of the PHSP premiums paid by the employer and the employee. Contact your organization’s group benefits provider or third-party administrator to issue this summary.

Again, only premiums paid by the employee qualify for tax credits.

Encourage employees to keep and file required paperwork

When preparing claims for tax credits on medical expenses, employees should have these documents ready:

-

receipts showing name of company or person who paid for the medical expense

-

prescription or written certification issued by a medical practitioner for certain medical expenses

-

Disability Tax Credit Certificate (Form T2201) for certain medical expenses

It’s best that employees keep clear copies, original and digital, of these documents on record. These need not be sent with the tax return, but the CRA might ask to see them later.

Educating employees on CRA-approved medical claims

While an employer is not responsible for their employees’ tax returns and compliance, it’s still good practice to educate them on tax issues. Consider this part of your organization’s financial literacy efforts.

Some examples of what you can do:

- Organize a training session on taxes and medical benefits

- Get checklists and infographics ready for your employees to use as guides

- Invite a financial expert to lead a session on taxes and personal finance

These efforts could have a lasting impact on your workforce. This strategy can:

- help reduce the financial stress your employees face

- promote higher employee engagement

- lead to better benefits uptake

Let’s go over these points in more detail:

Helps reduce financial stress

The stress from medical expenses can take a toll on employees. Knowing that there are benefits through the company’s PHSA or HSA will help ease their financial worries.

Knowing that tax credits are also available for a range of medical expenses can be a huge stress reliever.

Promotes higher employee engagement

Employees tend to be more energized and engaged at work when they feel that their employer is taking care of them. Seeing their employer host tax literacy sessions and workshops builds a sense of goodwill and loyalty among employees.

Leads to better benefits uptake

If employees are aware of the benefits they’re entitled to, there’s a higher chance that they’d use it! Look into the option of including voluntary add-ons in benefits. This might lead to higher usage of your benefits plans.

The bottom line on eligible medical expenses

Many employees may be missing out on valuable tax credits simply because they aren’t aware of what qualifies. From home renovations to service animals and gluten-free food products, the range of claimable expenses is broader than most people think.

HR teams can play a key role in raising awareness, offering guidance, and supporting employees with the right documentation. By doing so, organizations empower their teams to make better financial decisions and get more value from their existing benefits.

For more articles like this one, read and bookmark our section on compensation and benefits.