In contrast to last month, the general decline of available jobs has touched virtually all of the Canadian economy. July saw available jobs fall to their lowest level of 2024, with only two industries posting any year-over-year vacancy growth. Employee numbers, however, continued to rise, marking a decisive shift from labour scarcity to selective hiring.

STRATEGIC HR, OCTOBER EDITION

Available jobs continue to tumble, now impacting all but two industries; strong wage growth in surprising areas

In contrast to last month, the general decline of available jobs has touched virtually all of the Canadian economy. July saw available jobs fall to their lowest level of 2024, with only two industries posting any year-over-year vacancy growth. Employee numbers, however, continued to rise, marking a decisive shift from labour scarcity to selective hiring.

This selectivity is reshaping wage and workforce dynamics. Median wages remain historically strong but flat for a third straight month. With inflation creeping upward, real purchasing power has narrowed. Yet pockets of intense wage growth persist in specialized and high-skill sectors, even as those same industries post declining job openings. Tenure was shortened again in finance, construction, and public administration, suggesting that pay alone is no longer stabilizing retention, while litigation activity surged across provincial borders regarding safety, licensing, and professional standards bodies.

The national workforce, meanwhile, continues to expand, driven by gains in Alberta and Quebec and robust city-level growth in Calgary and Winnipeg. Joblessness remains highest among early-career workers, while educated candidates are also widely available. For HR leaders, the month’s data points to more candidates, slower turnover, and higher expectations for pay precision, managerial quality, and procedural fairness.

Executive overview

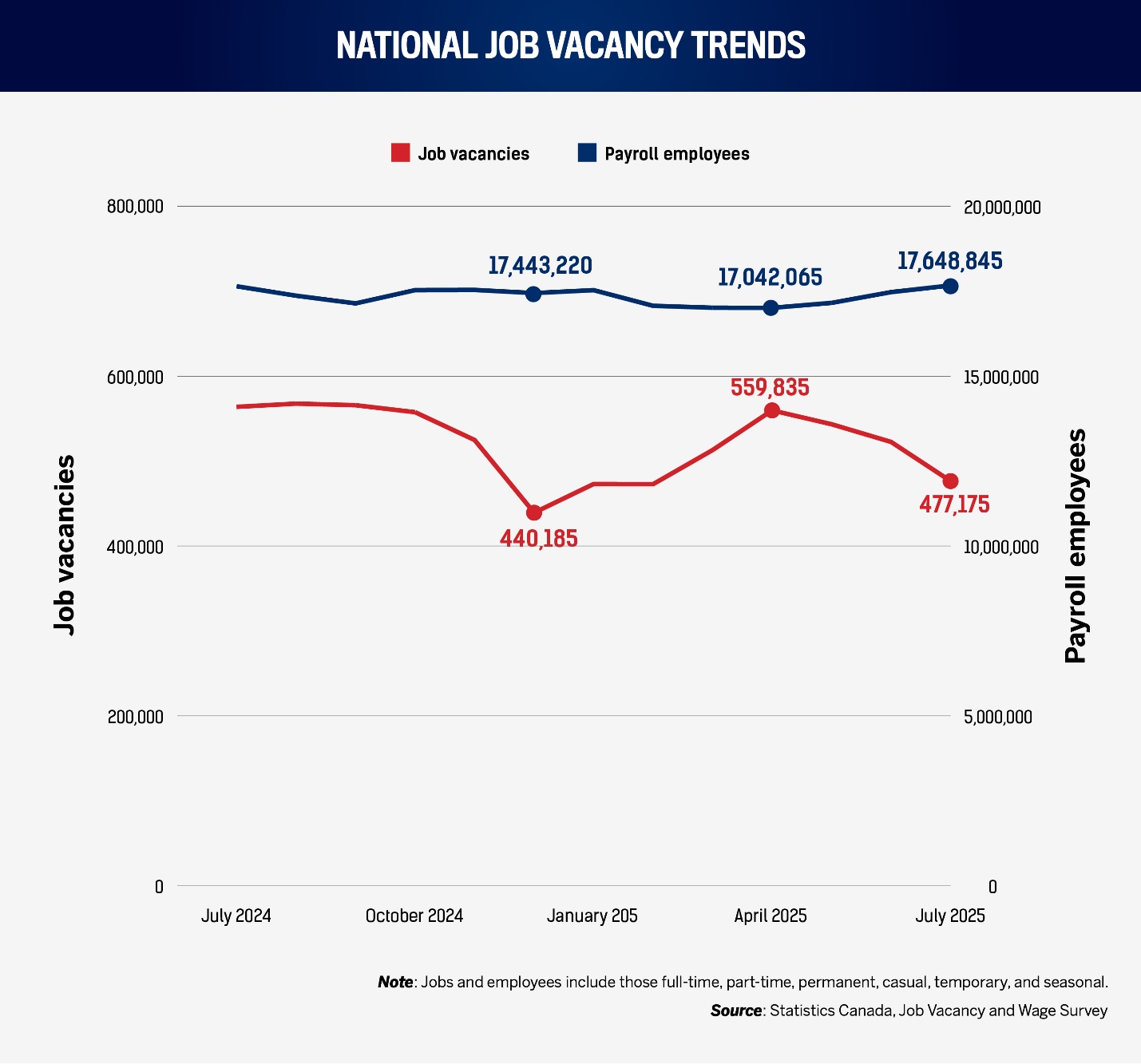

National job vacancy trends: New jobs continue to tumble, hit 2024 lows

- Vacancies fell to 477,175 in July (−45,770 month-over-month; −86,780 year-over-year, YoY), while payroll employment rose to 17,648,845 (+179,930 MoM; +21,845 YoY).

- The national vacancy rate fell to 2.6 percent in July from 2.9 percent in June and 3.1 percent in July last year.

- This was the result of July posting the fewest available jobs since January of this year.

- HR implication: expect larger candidate pools per requisition and longer shortlists as job vacancies continue to tumble; consider structured screening to separate the right fit from the sheer volume of applicants.

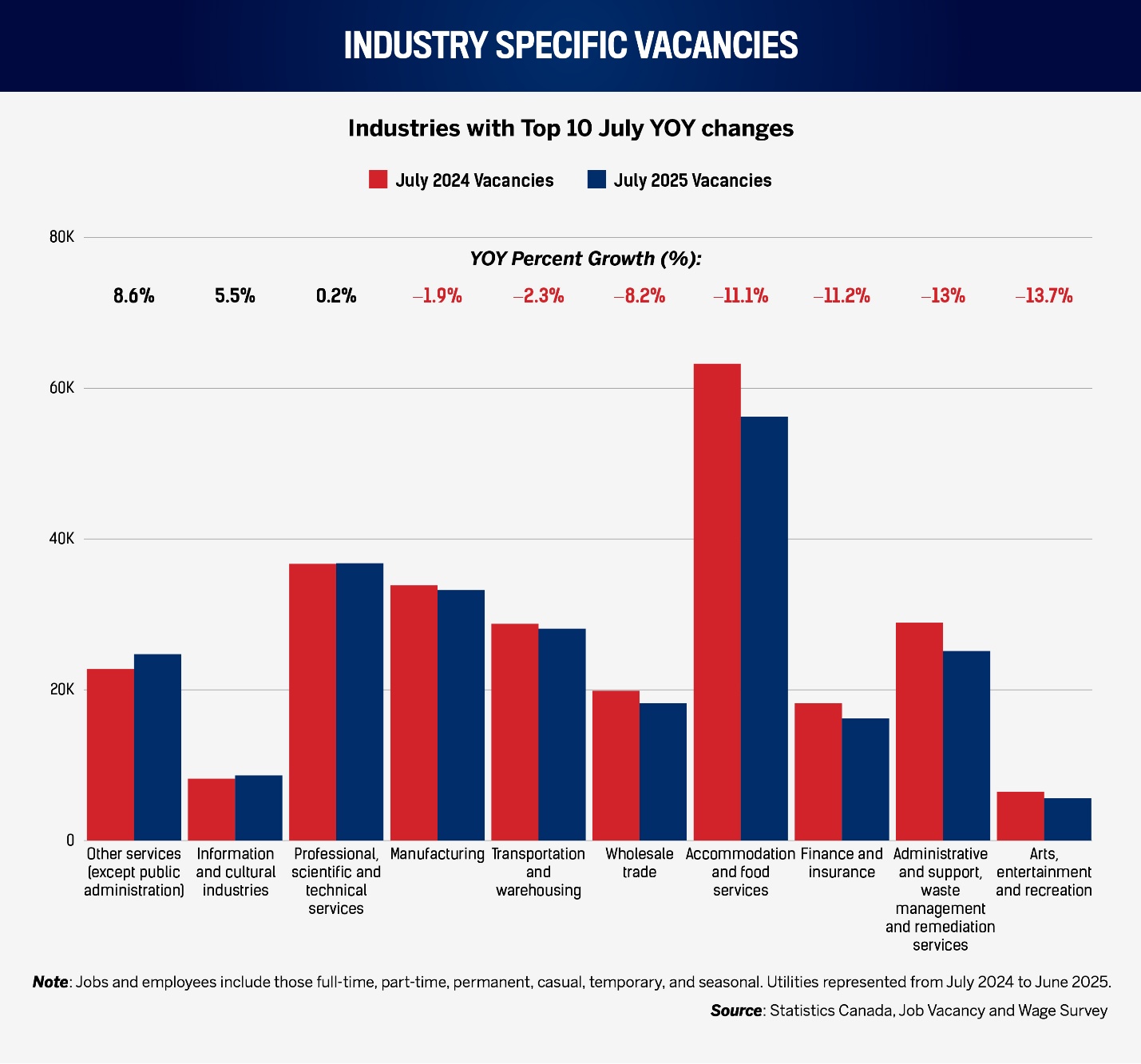

Industry-specific vacancies: Only two sectors buck the general downtrend

- In July, only two industries posted YoY vacancy-rate growth: other services (+8.6 percent, vacancy rate 4.1 percent) and information and cultural industries (+5.5 percent, 2.4 percent).

- Most sectors posted dramatic YoY declines in vacancies, especially in the goods-producing sectors. Surprisingly, closed doors include finance and insurance (−11.2 percent, 1.8 percent) and utilities (−27.9 percent, 1.2 percent).

- HR implication: Redeploy recruiters toward the few growth pockets; elsewhere, prioritize quality and internal mobility over backfilling.

- Notwithstanding the two growth pockets, expect fewer counteroffers, especially in the goods sectors. Use this window to close hard-to-fill specialist roles.

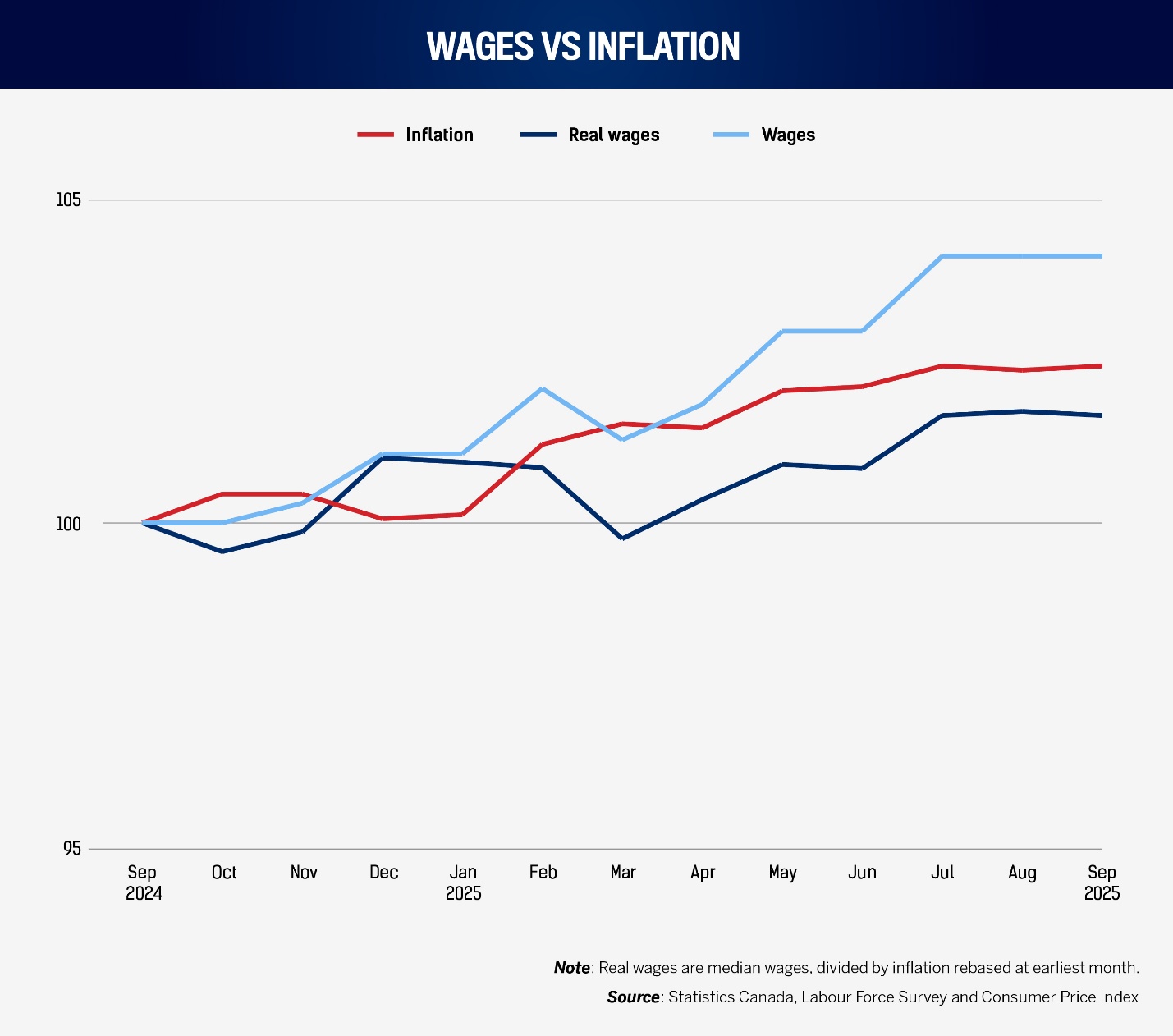

Wages vs. inflation: Real gains narrow as inflation ticks and median wages are unmoved

- Median hourly wages stayed at $35.00 in September, up $1.35 YoY (+4.0 percent) but unchanged from last July and August.

- CPI increased from 161.1 to 164.9 over the year (~+2.36 percent); real wages thus improved by about $0.54 at the median. YoY, this September, real wages fell back below inflation.

- Real purchasing power rose even as hiring became more selective, keeping candidate expectations firm.

- HR implication: sub-3 percent merit budgets continue to underwhelm; in payroll, prioritize differentiated awards and cost-of-work benefits.

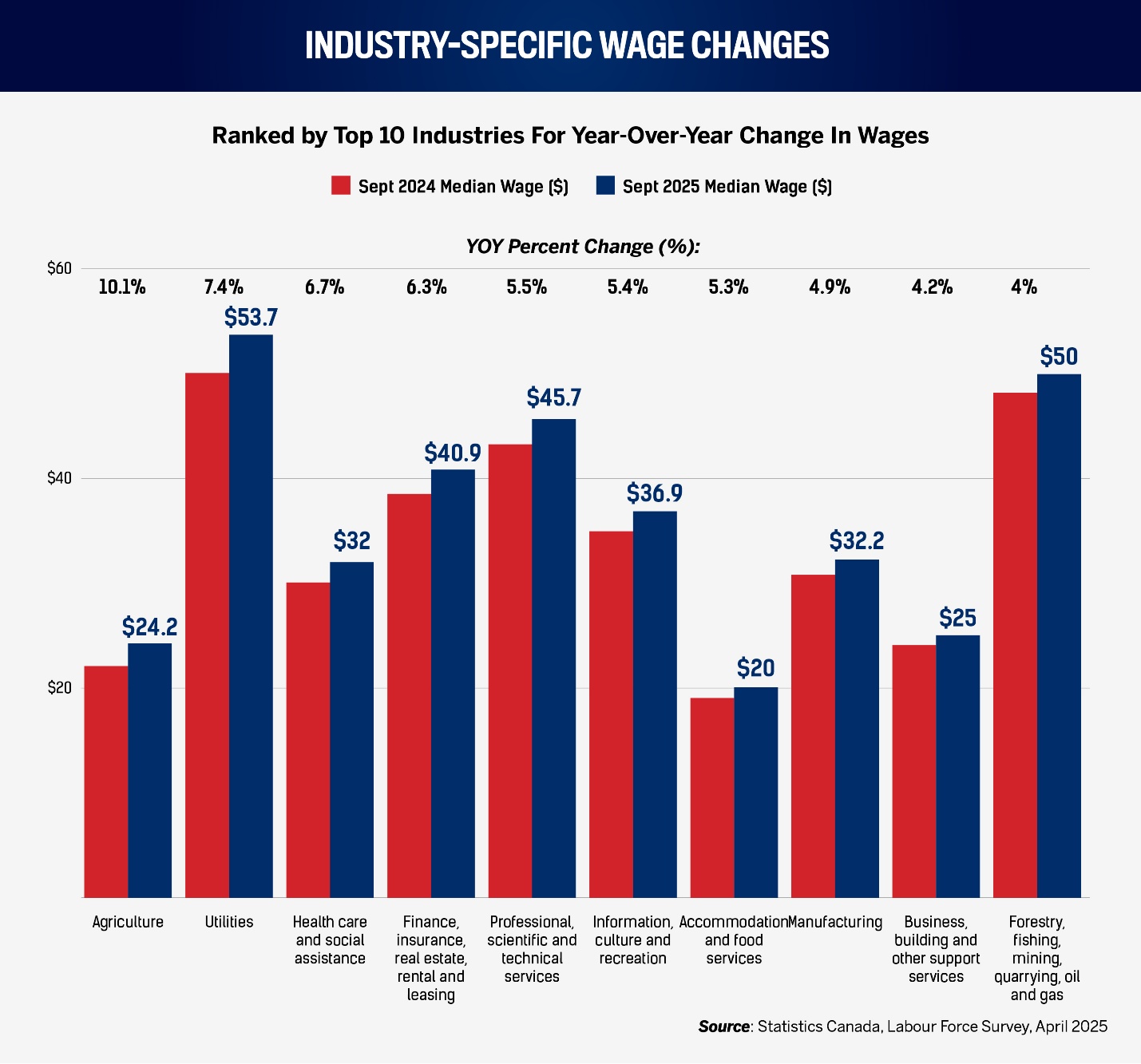

Industry-specific wages: Specialized fields lead wage growth even as jobs shrink; unusual slowdown in certain sectors

- September’s top three industries for YoY wage growth were agriculture (+10.1 percent), utilities (+7.4 percent), and health care (+6.7 percent), followed by finance and real estate and professional and technical jobs. Remarkably, information and culture posted its first modest YoY wage increase in months.

- Growth spans both operational and credential-intensive work, compressing differentials between entry-level and mid-tier roles.

- HR implication: monitor compression closely; refresh job architectures where rising floor pay is crowding mid-bands.

- Expect continued wage firmness in knowledge and critical infrastructure roles despite softer vacancies elsewhere. Those hiring in the information industry should look for further indication to ease the throttle on wage increases.

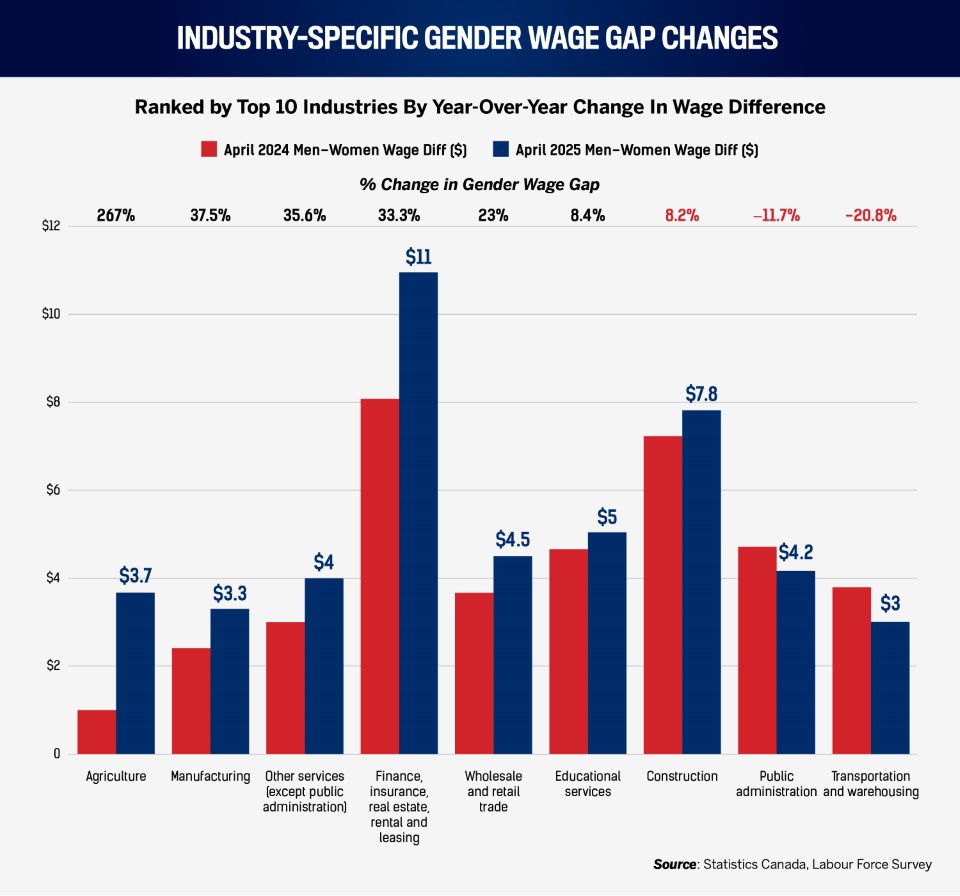

Industry gender wage gaps: Agriculture and finance reopen the gap; culture sees relief

- This month, agriculture jobs recorded another major gender pay gap increase, followed again by utilities and finance.

- Most other major sectors narrowed their gaps, including information and culture, transportation and warehousing, and public administration.

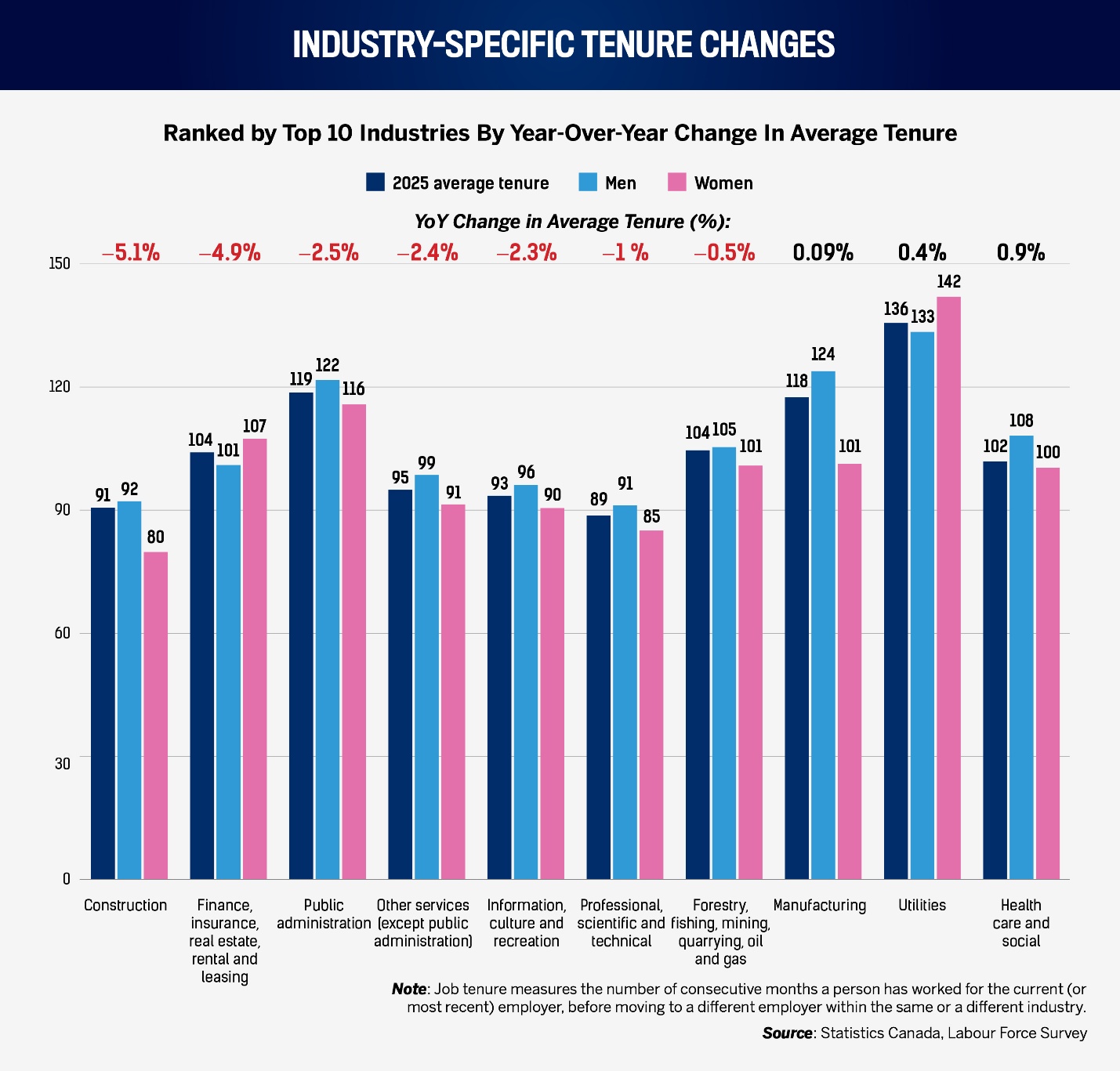

Tenure: Retention weakens in high-governance sectors, despite pay rises

- Tenure declines were concentrated in construction (−5.1 percent YoY to 90.6 months), finance/insurance/real estate/rental and leasing (−4.9 percent to 104.1), public administration (−2.5 percent to 118.7), other services (−2.4 percent to 95.0), information and culture (−2.3 percent to 93.5), professional services (−1.0 percent to 88.7), and forestry/mining/oil and gas (−0.5 percent to 104.6).

- Few industries improved meaningfully; most others were broadly stable.

- HR implication: wage growth alone is not stabilizing retention where schedules, safety, or change fatigue loom large.

- Focus on supervisor capability, predictable rosters, and 12–18-month internal mobility to arrest early attrition.

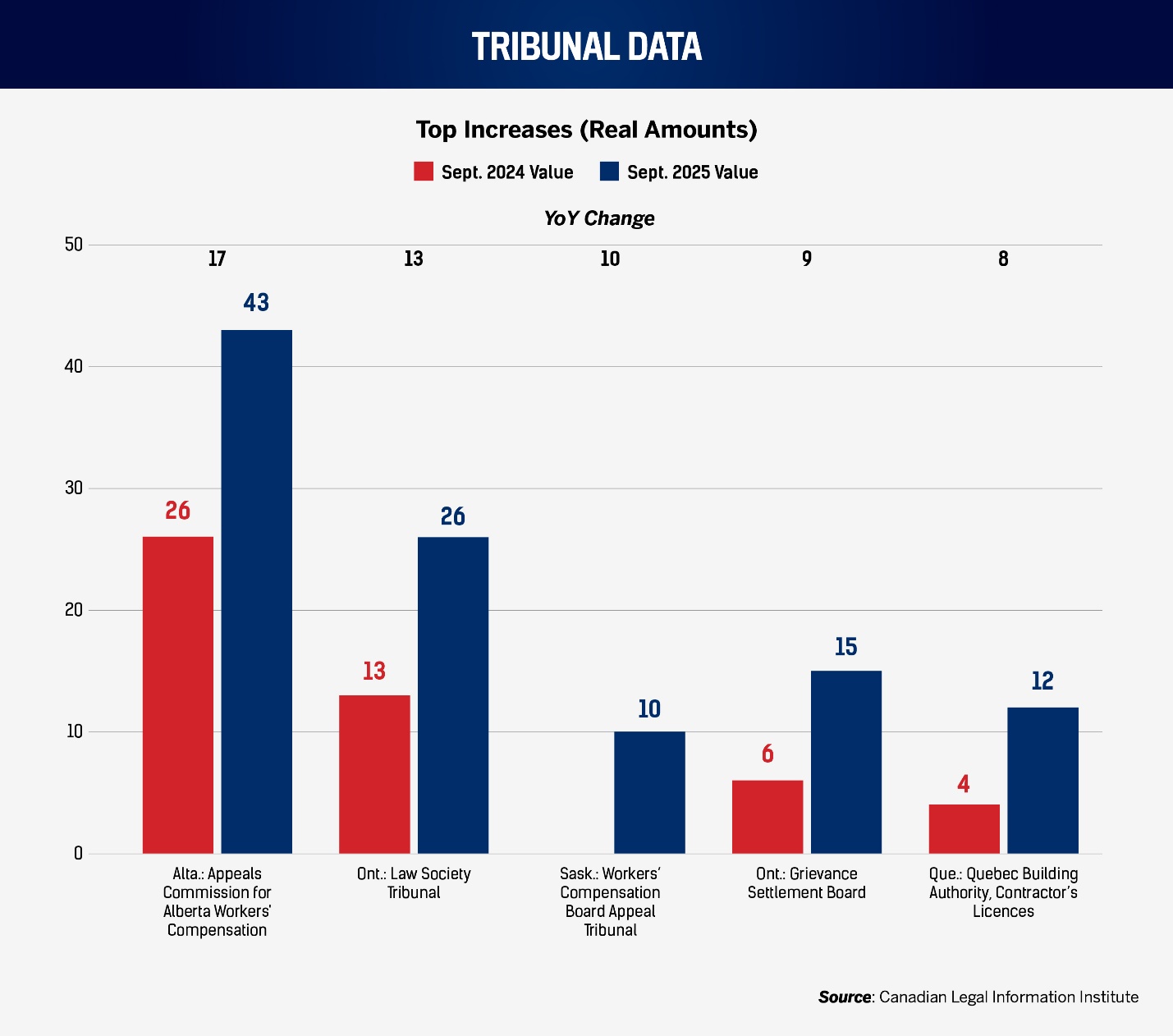

Litigation: Professional standards and safety cases are highlighted across provinces

- September’s additional YoY cases in Alberta, Ontario’s law society, and Saskatchewan clustered around return to work, earning-capacity determinations, procedural fairness, professional standards, and licensing compliance.

- Construction-adjacent employers should ensure contractor onboarding extends code-of-conduct and safety/accountability to sub-trades.

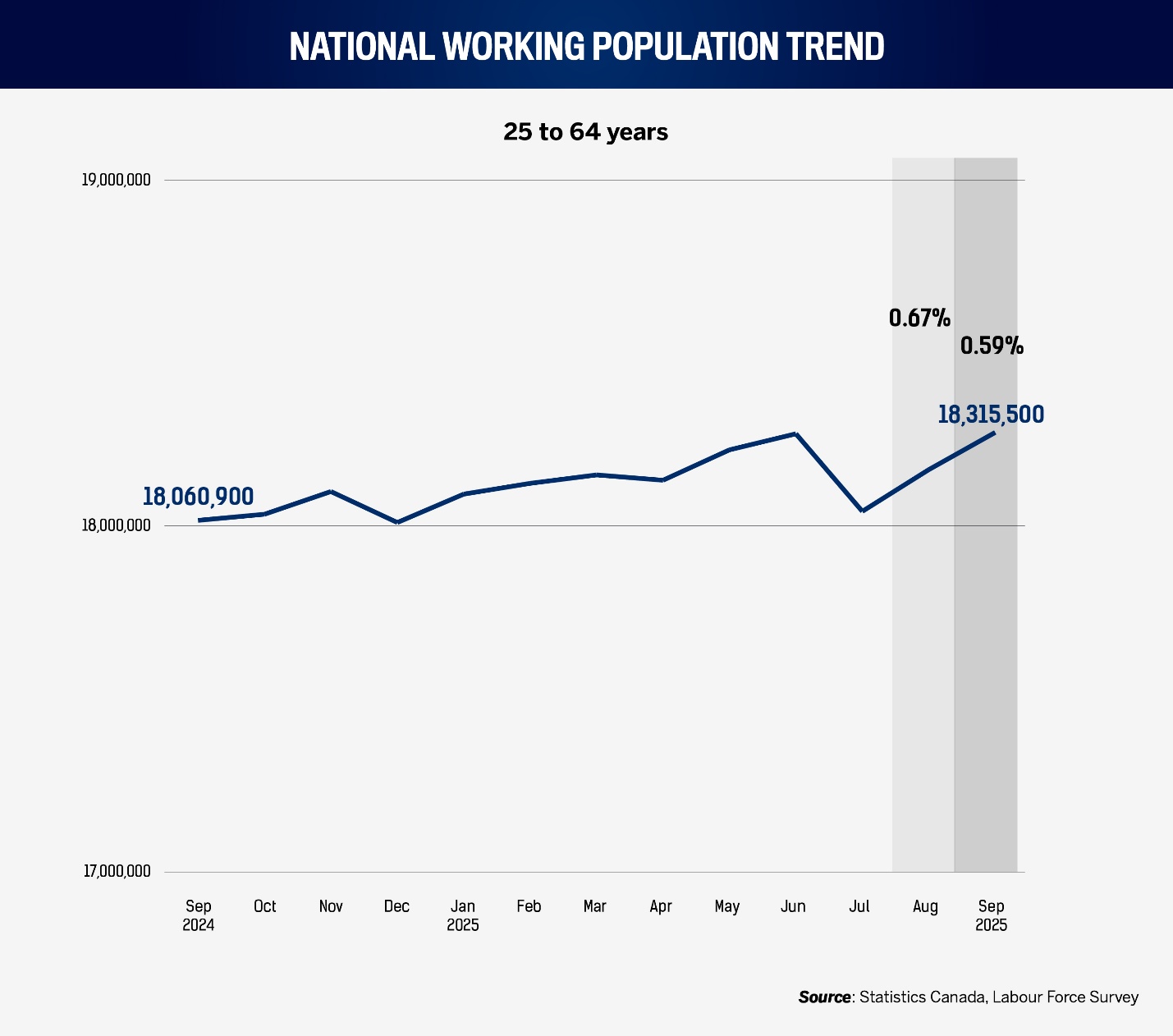

National workforce trends: Labour supply expands, but employers hire for certainty

- Canada’s core-age (25–64) labour force reached 18.315 million in September, up 107,800 month-over-month and 254,600 YoY.

- The supply tailwind is real; absorption is selective, as vacancy rates ease but payrolls expand.

- HR implication: map adjacent skills and design short reskilling paths to convert supply into capability.

- Build pipelines in sectors with durable vacancy or wage pressure (Sections 1B and 2B).

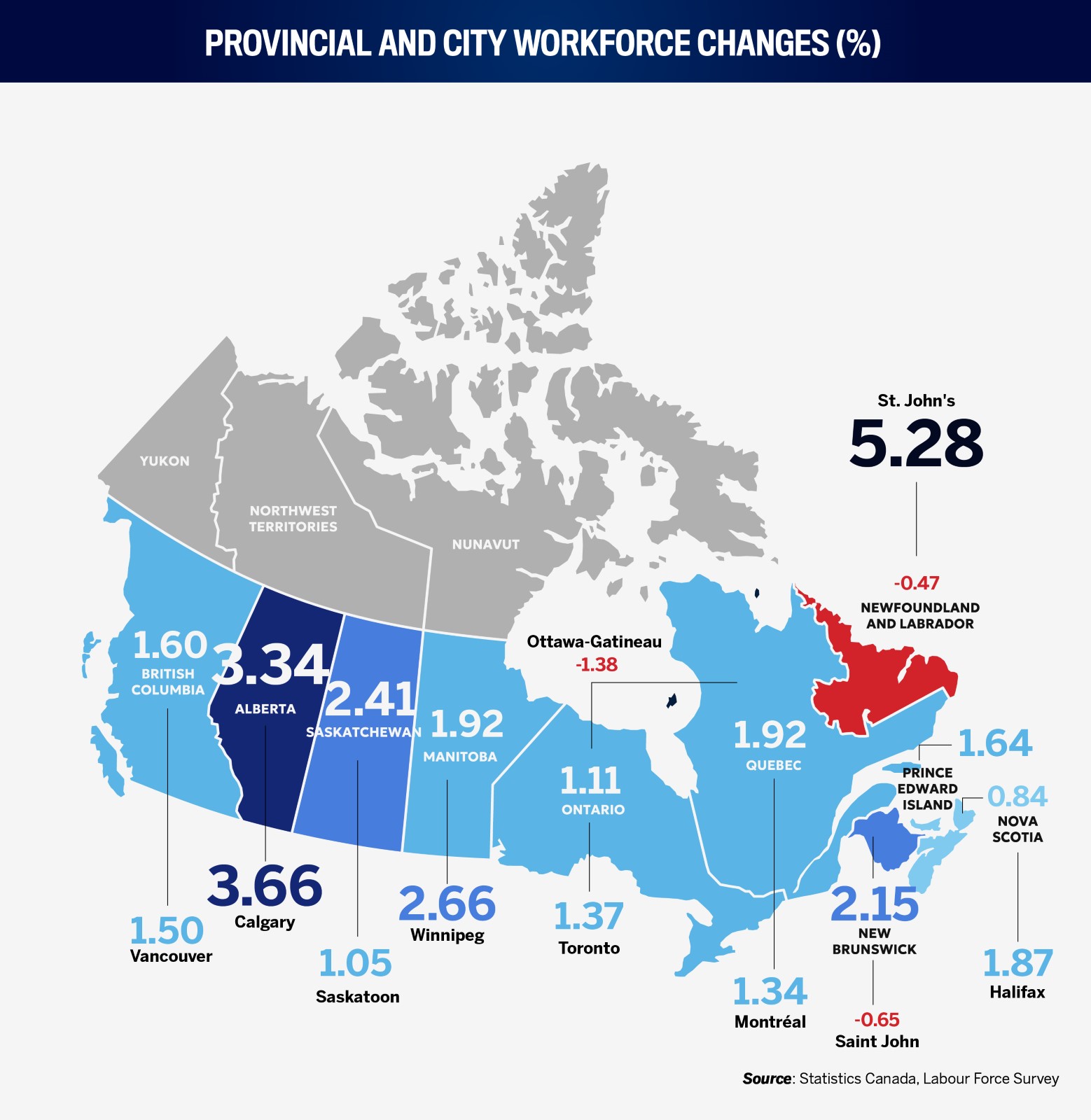

Provincial and city workforce changes: Prairies and Quebec power growth; Calgary leads the cities

- Workforce growth remains strongest in the Prairies and Quebec, with Alberta leading both in scale and pace; Calgary continues to post impressive workforce growth.

- Winnipeg and St. John’s outpaced their provinces in relative growth.

- HR takeaway: adopt a multi-hub recruitment model and widen remote eligibility to tap emerging urban labour pools while maintaining flexibility in slower-growth centres.

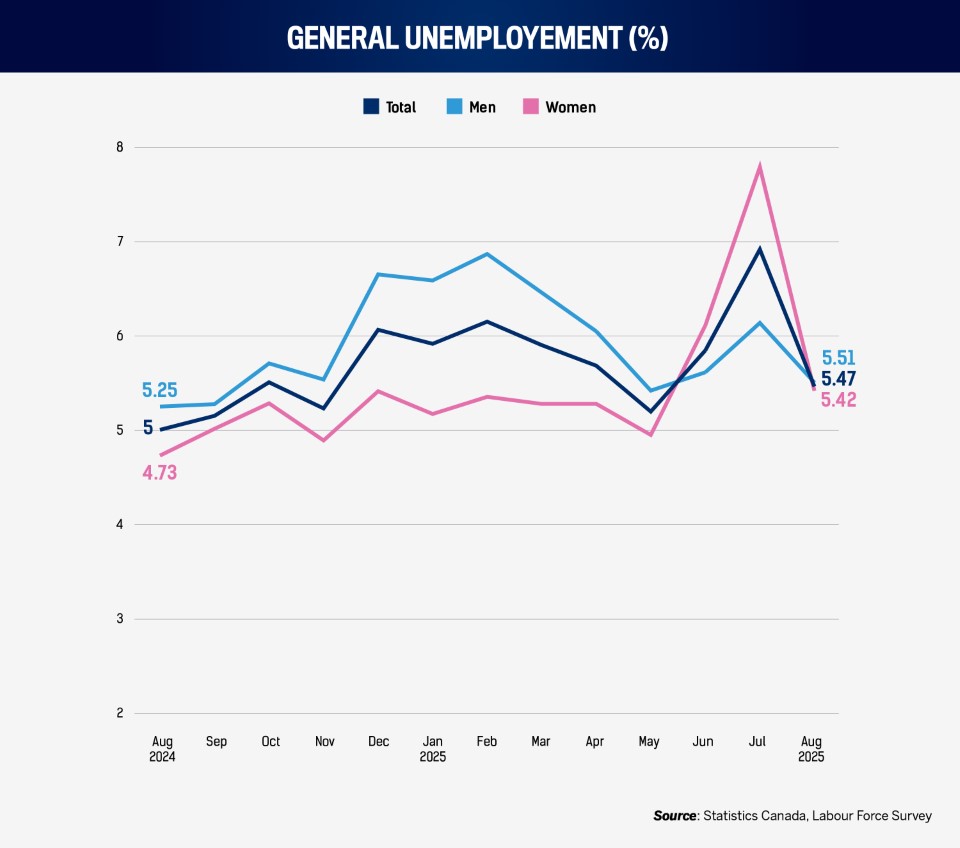

National unemployment trends: Unemployment returns to normal

- Core-age unemployment in September was 5.0 percent; men 5.3 percent, women 4.7 percent.

- The gap is modest and reverses the sharper female joblessness noted in recent months.

- HR implication: expect steady application volumes from both cohorts; keep bias mitigation active in screening as volumes rise.

- Maintain transparent pay and promotion criteria to protect equity gains while competition for roles increases.

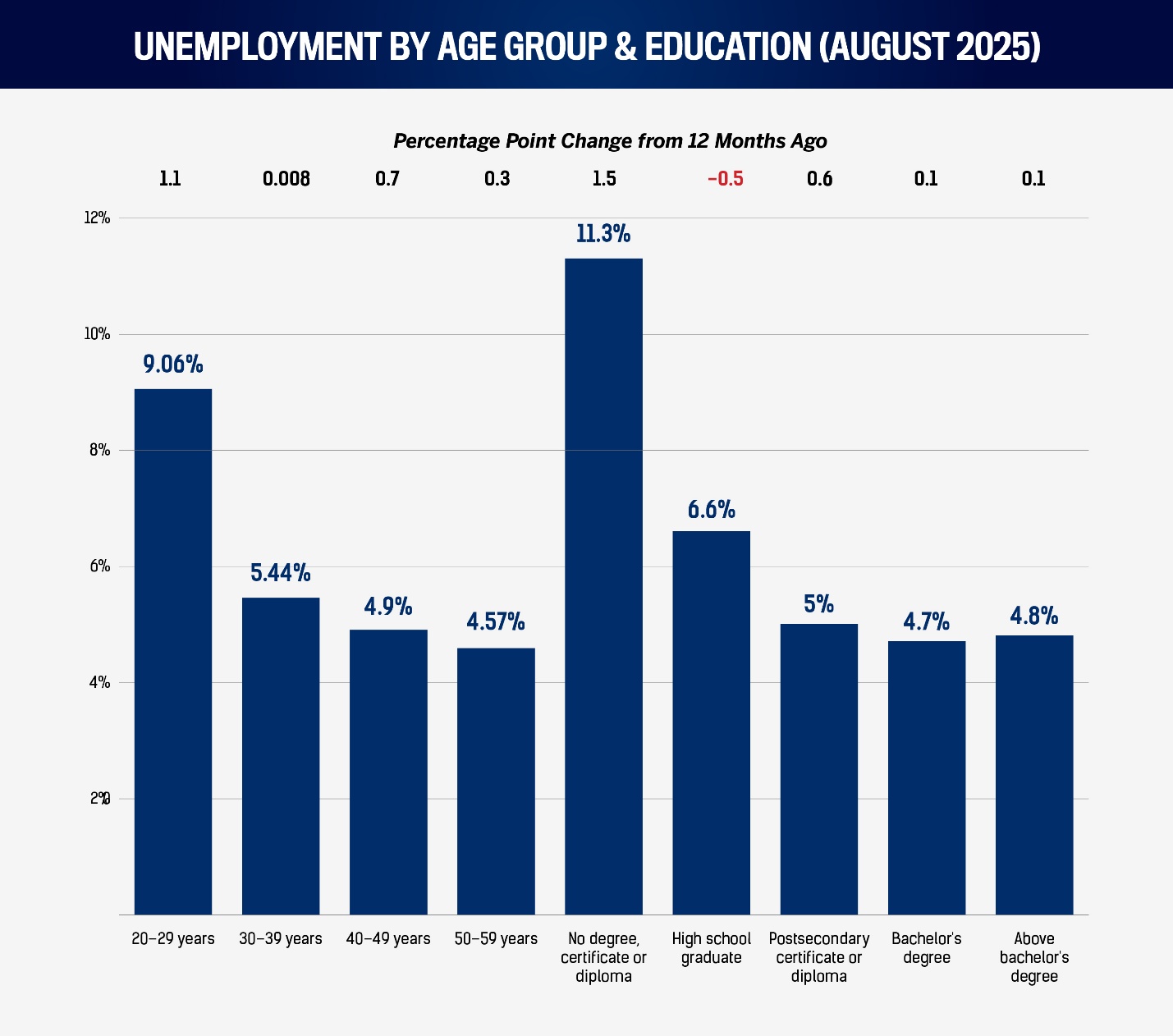

Unemployment by age and education: Early-career joblessness persists; educated candidates abundant

- By age (September): 20–29 at 8.0 percent; 30–39 at 5.4 percent; 40–49 at 4.2 percent; 50–59 at 4.3 percent.

- By education (September): no credential 9.8 percent; high school 7.1 percent; postsecondary certificate/diploma 4.4 percent; bachelor’s 4.6 percent; above bachelor’s 4.6 percent.

- HR implication: early-career remains the most exposed; mid-career jobseekers are numerous enough to support selective hiring; highly educated candidates are available at reasonable cost if work is meaningful.

- Prioritize “returnships” and re-entry cohorts (three to six months) for displaced professionals; map adjacent skills to avoid over-specification.

1. Job vacancies

National job vacancy trends: New jobs continue to tumble, hit 2024 lows

This July, Canada’s job vacancies continued to tumble. The number of available jobs slipped to 477,175, down 45,770 versus June and 86,780 below last July, to their lowest since February this year. The number of employees nevertheless climbed 179,930 month-over-month and 21,845 year-over-year (YoY) – compared with the past 12 months, that was a higher month-to-month addition of new employees. These movements brought the vacancy rate down to 2.6 percent in July, from 2.9 percent in June and 3.1 percent a year earlier. The combination (far fewer open posts but many more employees) suggests the cooling of fervent hiring activity; many employers are pausing general backfilling while moving ahead on roles with a clear return on investment.

For HR teams, that means more applicants per opening and a wider spread of quality. Build a two-step assessment (short, skills-relevant task followed by a structured interview rubric) to maintain speed without compromising fairness. In the scant areas where vacancy rates are cooling but hiring opportunities have grown YoY (for instance, in corporate services, see below), consider converting contractors into staff to capture value from the expanding pool while controlling fixed costs.

Cross-references: These trends align with September’s wages-versus-inflation picture (Section 2), where purchasing power still nudges up, and with tenure declines in several service and knowledge sectors (Section 3), suggesting firms are using this moment to reprofile roles and tighten performance expectations.

Industry-specific vacancies: Only two sectors buck the general downtrend

In this report’s previous edition, the total job vacancy decline was led by opportunity declines in three-quarters of the economy: 15 of 20 industries. Come July, YoY, opportunities have receded in all but two industries.

Of these two industries, other services (which include personal care, repair, and community organizations) posted the strongest YoY job vacancy increase (+8.6 percent, up to 24,690), followed by information and cultural industries (+5.5 percent, 8,600).

Beyond these, available jobs were flat to lower everywhere, including professional, scientific, and technical services (broadly stable near 2.9 percent), finance and insurance (down to 1.8 percent), utilities (down to 1.2 percent), and accommodation and food (down to 4.0 percent).

In July, the agriculture, company management (jobs include executives, corporate planning, and accounting), and mining industries posted the greatest YoY opportunity declines, falling 41 percent, 37 percent, and 31 percent to just 6,925, 1,510, and 3,580, respectively.

The practical upshot: move decisively in the two growth pockets and in any sub-sector where your own pipelines show persistent scarcity (e.g., niche content, data, or field service roles). In sectors with declining vacancy rates, resist blanket pay compression; use the moment to improve hiring quality, raise bar-raising thresholds, and consolidate temporary and permanent staffing plans. As September’s edition cautioned, sharp rebounds can follow short plateaus in specialist markets; keeping an active passive-candidate bench now avoids a scramble later.

2. Wages

Wages vs. inflation: Real gains narrow as inflation ticks and median wages are unmoved

Pay continued to outpace prices in September. The median hourly wage remained at $35 for a third month, up $1.35 YoY (+4 percent). Over the same period, CPI rose from 161.1 to 164.9 (~+2.36 percent). This implies that YoY, real wages grew by only $0.54. Unlike the previous month’s edition, YoY, real wage growth was thus recorded as lower than inflation itself. Employees will feel that in their weekly budgets, and candidates will anchor to it during offers.

For HR, two points follow. First, where budgets constrain base pay, protect differentiation: use sign-on awards and accelerated progression for scarce skills, and fund benefits that reduce out-of-pocket costs (transport and mental health coverage) to enhance total reward without locking in high fixed pay. Second, keep one eye on the few sectors where vacancy growth persists (other services and information and culture industries, outlined above). Even when overall vacancies ease, wage competition remains in pockets tied to content, data, and customer service delivery.

Industry-specific wages: Specialized fields lead wage growth even as jobs shrink; unusual slowdown in certain sectors

As agriculture’s available jobs have fallen dramatically the past two months, its recent remarkable median wage increase underscores the retention of high-value positions and possibly formalization and technology adoption along the value chain. Utilities, health care, and professional services posted relative YoY wage increases in great excess of last month, increasing pay for skill depth, governance, and regulated delivery. It’s worth noting that this month’s greatest YoY wage increases occurred in highly specialized fields with shrinking job opportunities.

Also noteworthy: for the first time in the past several months, information and cultural industries’ YoY wage growth was modest, just 5.4 percent, compared to months of leading and double-digit relative increases. Wages there remain elevated and consistent with ongoing demand for content and product talent. Next, accommodation and food gains will keep pressing supervisors’ differentials unless mid-band ranges are refreshed.

HR leaders: where floor pay has risen fastest, revisit job families, pay progression, and allowances to ensure that supervisors and technical leads maintain headroom. Align retention levers to the work: for utilities and professional services, invest in credential funding and project rotations; for agriculture and accommodation, predictability of shifts and safer, better-tooled workstations often buy more loyalty than another 50 cents on the hour.

Industry gender wage gaps: Agriculture and finance reopen the gap; culture sees relief

In September, eight industries widened their gender gaps (down from nine the previous month), and several large employers narrowed theirs. In finance and allied real estate services, for example, higher-paying specialisms can lift the male median faster if women are underrepresented in those niches. In manufacturing and other services, team lead or maintenance roles can have similar effects.

Information and cultural industries, which led the YoY gender wage gap increase for several months, showed reprieve as the gap fell from $5.5 to $4.08 YoY. Since this industry’s general wage growth has also fallen, this virtually proves that women have been largely left out of the industry’s greatest wage gains in recent months. Likewise with agriculture’s dramatic increase, but instead considering the limited job availabilities in that industry and where high-value roles have been retained.

Run targeted equity audits in the seven widening sectors, focusing on new-hire rates, internal moves, and the distribution of allowances and premiums. Where your sector narrowed gaps this year, lock in the gains: standardize starting-pay guides, expand diverse slates for the few roles that disproportionately influence the median (e.g., senior technicians and underwriters), and track promotion cycles for symmetry’s sake.

3. Tenure and litigation

Tenure: Retention weakens in high-governance sectors, despite pay rises

The industries with the heaviest project cadence and governance demands saw the sharpest tenure erosion. Construction’s 5.1 percent drop to 90.6 months and finance/real estate’s 4.9 percent fall to 104.1 months suggest that pay raises (Section 2) are not yet offsetting pressure from workloads, re-platforming, and regulatory remediation. Public administration’s decline, though smaller, is notable given its historic stability.

Retention lift in these environments rarely comes from base pay alone. Stabilize schedules where possible; fund supervisor training in coaching, conflict resolution, and workload planning; and build short, credible internal pathways that move high-potential performers into more stable roles within a year. Where tenure is flat but applicant volumes are up (Sections 1 and 6), use the breathing room to reset performance expectations and tighten probation frameworks to reduce downstream remediation.

Litigation: Professional standards and safety cases are highlighted across provinces

Alberta (Workers’ Compensation Appeals): September’s additional decisions frequently turned on pre-existing conditions, the causal link between work and injury, entitlement to wage-loss benefits (including interim relief), and earning-capacity assessments. Several matters addressed return-to-work suitability (e.g., cashier or receptionist roles) and whether symptoms prevented resumption of pre-accident employment. The pattern underscores the value of well-timed functional abilities forms and contemporaneous offers of modified work.

Ontario (Law Society Tribunal): Cases ranged from trust-account violations and client-fund misapplication to professional-conduct failures (harassment and integrity) and procedural issues (redactions and videoconference practice). For legal and compliance employers, governance must exceed minimums and include regular file audits, conflict checks, and respectful-workplace refreshers to reduce regulatory exposure.

Saskatchewan (WCB Appeal Tribunal): A number of additional September matters addressed temporary aggravations versus permanent impairments, reinstatement of wage-loss benefits, vocational rehabilitation and training sponsorship, and whether internal employer investigations constituted compensable psychological injury. The tribunal emphasized medical evidence, mitigation of earnings loss, and cooperation with rehabilitation plans. Early contact and clear RTW plans remain decisive.

Ontario (Grievance Settlement Board): Decisions covered overtime assignment, classification disputes, disclosure (including access to clinical notes), harassment and medical-leave issues, and preliminary time-limit rulings. These remind HR that case management basics, i.e., timely disclosure, documentation of accommodations, and consistent application of overtime and classification rules, are both compliance and retention levers.

Quebec (Building Authority): Licensing-compliance decisions cited license status, bankruptcies and unpaid debts, and scope-of-work issues across construction subcategories (including electrical). Employers should verify that subcontractor licenses and “répondant/responsable” designations remain current and that corporate probity requirements are met before site mobilization.

September’s edition flagged Ontario’s sustained caseload pressure; this month’s distribution confirms that risk is not confined to labour boards. Professional standards bodies and safety/licensing authorities in the province are highly active. Tighten internal audit cycles and ensure documentation standards are understood and practicable for frontline leaders.

4. Workforce

National workforce trends: Labour supply expands, but employers hire for certainty

September’s 18.315 million core-age labour force caps a year of steady growth, returning the labour force to recent highs following a sharp July dip. With vacancies easing and employees rising, employers appear to be moving cautiously, hiring for certainty rather than coverage. This is a favourable environment for skills-based hiring: broaden requirement statements, replace “X years in Y industry” with verified skills and validated tasks, and stand up short reskilling curricula where your roadmap allows 6–12-month transitions (e.g., retail multi-unit supervisors into field operations; manufacturing quality technicians into utilities inspection).

Provincial and city workforce changes: Prairies and Quebec power growth; Calgary leads the cities

The geography of growth remains favourable to the Prairies and Quebec. Alberta’s combination of scale and percentage growth, across both its metropolitan hub and the province, makes it the prime secondary hub for national employers. Calgary’s city-level momentum offers credible alternative landing zones for roles that do not require the Toronto or Vancouver ecosystems. Meanwhile, Winnipeg’s gains, though more modest in absolute terms, provide operational depth and lower bidding pressure for experienced supervisors and analysts. This month, it and St. John’s were the only major cities to rapidly outpace their provinces for relative workforce growth.

Deploy multi-hub requisitions (e.g., Toronto and Calgary; Montréal and Winnipeg) and widen remote-eligible footprints where feasible. For Ottawa–Gatineau and Saint John, differentiate through career-path clarity and flexible arrangements, particularly in public-sector-adjacent and industrial roles, to offset softer demand.

5. Unemployment

National unemployment trends: Unemployment returns to normal

The generation unemployment rate fell back to about 5.4 percent. This followed last month’s dramatic rise, which had been spurred by a spike in unemployment among working women ages 55 to 59 (66,000+).

The national unemployment rate is consistent with a market that is no longer overheated but is not weak. With vacancies easing and payrolls growing (Section 1), the mix suggests employers are hiring against crisper business cases. Ensure that structured interviews, skills-based tasks, and de-biased screening protocols are fully operational, particularly for high-volume roles where the temptation to fall back to “pattern-matching” is strongest.

Unemployment by age and education: Early-career joblessness persists; educated candidates abundant

Age patterns confirm that early-career workers bear the highest joblessness. Mid-career rates are moderate but, coupled with increased applicant volumes, provide an opportunity to upgrade team capability without inflating costs. Education patterns are strikingly flat above high school; unemployment for bachelor’s and above-bachelor’s sits near 4.6 percent. Employers can therefore access well-qualified candidates provided that the role content and progression are credible.

Age patterns confirm that early-career workers bear the highest joblessness. Mid-career rates are moderate but, coupled with increased applicant volumes, provide an opportunity to upgrade team capability without inflating costs. Education patterns are strikingly flat above high school; unemployment for bachelor’s and above-bachelor’s sits near 4.6 percent. Employers can therefore access well-qualified candidates provided that the role content and progression are credible.

Turn this into an advantage: define what potential looks like in your context (two or three observable skills), use short work-sample tasks to validate it, and offer concrete development routes. For entry-level roles, the tightest retention lever remains predictability of hours and supervisor quality; invest there first.

Closing guidance for HR leaders

Across October’s indicators, the same pattern repeats: hiring is slowing, but not stalling. Job vacancies have fallen to their lowest point this year, but payrolls and labour force participation continue to rise. Wages remain high but have stopped climbing, and real gains are narrowing as prices edge up. The overall result is a market that is still active but increasingly selective.

Several themes link the sections together. The sharp drop in vacancies connects directly to shorter tenure in construction, finance, and public administration, where these organizations appear to be reshaping roles instead of expanding headcount. Wage growth remains strongest in specialized sectors (utilities, agriculture, and health care) even as those same areas report shrinking job opportunities, showing that retention, not recruitment, is driving pay increases. The widening gender pay gaps in agriculture and finance also echo this wage concentration. Litigation trends mirror tenure patterns: the most active tribunals (those in Ontario and increasingly the prairies) are in provinces and sectors facing heavy regulatory or return-to-work pressures, reinforcing the need for consistent documentation and supervision.

The labour force is still growing, led by Alberta and Quebec, with Calgary and Winnipeg outpacing their provinces. Unemployment has returned to normal levels, but its makeup matters: joblessness is concentrated among early-career workers, while mid- and high-skill candidates are widely available. Together, these shifts indicate that employers have more choice, and employees face more scrutiny.

Guidance: With the market cooling unevenly, focus on quality, clarity, and balance. Match hiring pace to business certainty, update pay structures where compression is emerging, strengthen supervisory consistency, and use the expanded talent pool to fill roles more precisely. October’s Strategic HR in one direction: Canada’s labour market is steadier, not weaker, and offers a brief, useful pause for employers to rebuild alignment before the next cycle begins.