Employers committed to mental health should include financial health programs too

What’s the average amount of consumer debt employees are carrying?

$15,473, according to a 2017 Ipsos poll conducted for Global News. Considering the average salary in Canada is about $50,000, this level of debt is quite significant when compared to income.

Not surprisingly, 42 per cent of Canadians rank money as their greatest source of stress, causing them to lose sleep and to have increased anxiety, according to a 2014 survey by the Financial Planning Standards Council. This is significant when compared to 23 per cent of employees who ranked work as their number one source of stress.

Because of these kinds of dramatic numbers, the Total Health Index (THI) includes financial health in the life pillar. Employee productivity is impacted not only by workplace experience and mental and physical health but by financial health.

If someone is worried about money, it’s understandable to feel stressed about how to pay bills to obtain the essentials for healthy living, such as food and medicine.

Organizations that support and implement mental health strategies and programs typically do so to support two key imperatives: prevent mental injuries and promote mental health.

For employers committed to employees’ mental health, based on THI research findings, it’s recommended to include financial health.

THI research shows that about 55 per cent of employees report good financial health, 34 per cent strained financial health and 11 per cent poor financial health.

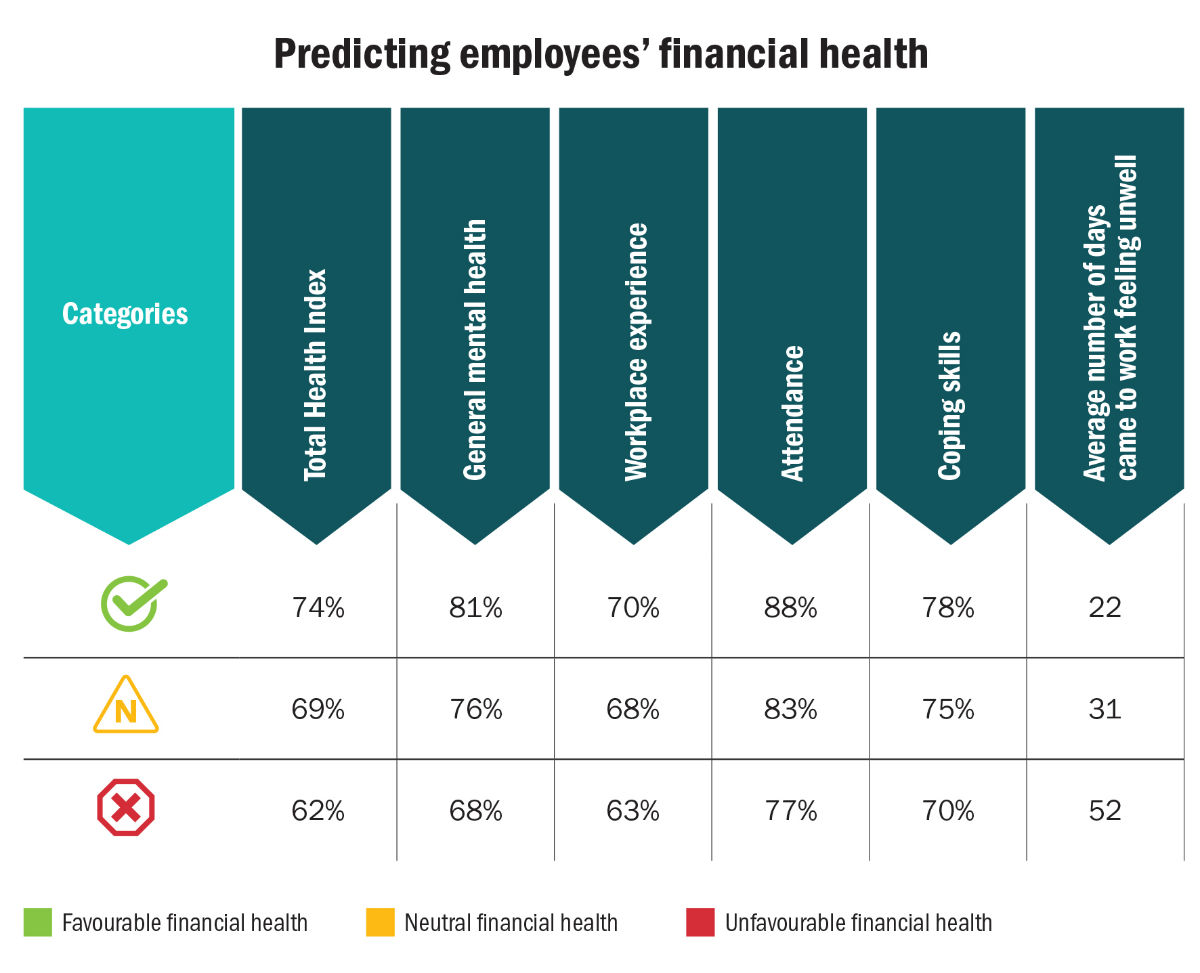

Cutting the data by the three categories reveals notable differences in employees’ THI scores. The mental health pillar is the number one driver in relative importance for predicting employees’ financial health.

The table to the right provides examples of how employees in each of the three financial categories compare in several areas that can predict health, engagement and productivity. Note: The higher the percentage score, the better.

Employees who have lower financial health report lower mental health than those who report good financial health.

What employers can do to support employees’ financial health:

- Evaluate the benefits of measuring employees’ financial health. It can be helpful to not only measure what the average employee is doing to promote their financial health (such as saving strategy, debt management and cash flow management) but also perceptions of their financial health and its influence on overall engagement and productivity. This information can assist in evaluating the effectiveness of current programs and identifying opportunities to support employees in need.

- Include financial health programs as a part of your mental health strategy (for example, prevention). This is one tactic to help employees with financial health concerns to acquire the knowledge and skills to make better decisions. Financial health issues may be due to ineffective decision-making (such as lifestyle shopping decisions) that can put employees at risk but if changed, could have a positive impact on their financial situation. Financial health issues may not be due to just a lack of money — they can result from ineffective spending and poor budgeting. Like with mental health, employees must learn how to own financial health to take charge of it.

- Educate employees on the kind of programs the employer has in place to support employees experiencing financial health issues (such as employee family assistance programs (EFAPs)). Don’t just tell employees about these programs through emails or the like — provide specific communications and examples that employees can relate to that capture their attention. As well, explain how financial health programs work, with respect to the kinds of experience employees can expect, and the tools available to assist with financial decisions (such as a budget).

- Don’t assume all employees have basic budgeting skills. There are three elements to budgeting: bills, future saving and discretionary spending. One effective way for employees to learn to take control of financial health is to put in place more controls around their daily decision-making, especially discretionary spending.

- Consider adding a short financial health module when onboarding new employees. Use this module to assist new employees who may not yet have developed the knowledge and skills to understand how to make a budget, how to leverage a tax-free savings account (TFSA) and how to make wise benefit decisions based on their current financial needs. Some new employees may not understand the real value of defined contribution (DC) matching contributions, for example. Don’t assume all new employees can navigate or will read and learn all the information that can help them make the best decisions when starting a new role.

Bill Howatt, Ph.D., Ed.D., is the Toronto-based chief of research and development, workforce productivity, at Morneau Shepell. For more information and education about the company’s Total Health Index (THI), please visit www.morneaushepell.com.